News: Microelectronics

11 May 2026

Wolfspeed’s quarterly margins and cash burn improved despite falling revenue

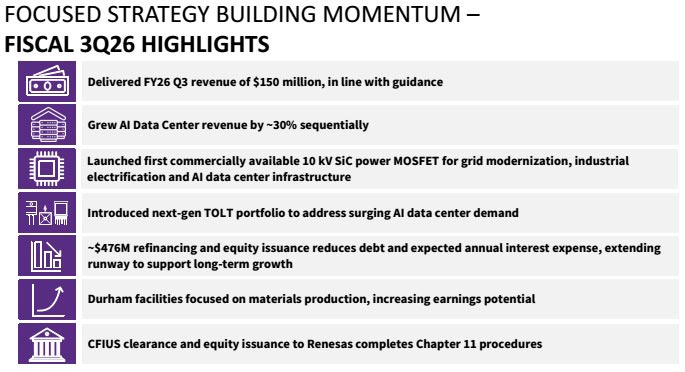

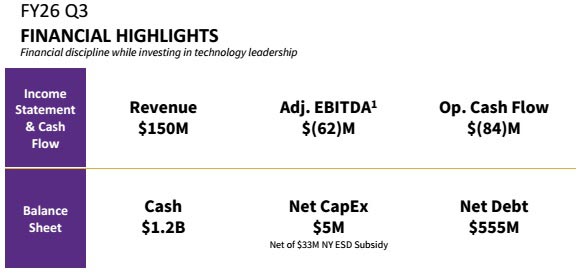

For fiscal third-quarter 2026, Wolfspeed Inc of Durham, NC, USA — which makes silicon carbide (SiC) materials and power semiconductor devices — has reported revenue of revenue of $150.2m, down 10.6% on $168m last quarter and 19% on $185.4m a year ago.

Materials Products revenue has fallen by 36% from $77.9m a year ago to $50.1m (driven largely by a tightening demand environment and increased competition in the market), but this is roughly level with $50.2m last quarter.

Power Products revenue was $100.1m (down 15.4% on $118.3m last quarter and 6.8% on $107.5m a year ago). Of this, 90% was from devices made at the 200mm-wafer Mohawk Valley Fab in Marcy, NY, compared with just 64% ($76m) last quarter. The remaining 10% was last-time-buy shipments of device inventory made at the 150mm-wafer Durham fab after its shutdown at the end of November, a month ahead of schedule. After growing by 50% sequentially last quarter, revenue from AI data-center applications grew further, by about 30% sequentially in fiscal Q3, reflecting a “moderate but expanding part of the firm’s business. Increasing customer engagement “gives us confidence in the long-term trajectory of this opportunity,” says interim CEO Robert Feurle. Business highlights during the quarter included:

- launching the first commercially available 10kV SiC power MOSFET for grid modernization, industrial electrification, and AI data-center infrastructure;

- introducing the next-generation TOLT portfolio to address growing AI data-center demand.

All device production has now shifted to 200mm wafers (at the Mohawk Valley Fab, opened in April 2022). Shutdown of 150mm-wafer device production at the Durham “creates optionality to redeploy that space,” says Feurle. So, the Durham site is now dedicated to materials production and supporting near-term growth, including commercial-scale 200mm wafers development. “This approach allows us to increase output and improve our earnings potential by leveraging our current tooling base, without heavy incremental capital investment that would otherwise be required,” he adds. “The Durham campus can currently support all commercial materials activities as well as our emerging trend and user platform.”

“We are also leveraging AI within our own operations,” notes Feurle. “Through our expanded partnership with [US-based] Snowflake, we have unified factory, supply chain, and enterprise data on a single platform and deployed AI-driven tools that enable real-time insights and faster decision-making across the organization.”

Margins and cash burn improved

On a non-GAAP basis, gross margin was –20.6% (compared with 2% a year ago), due mainly to a $46m impact from ongoing under-utilization of the manufacturing footprint. However, this was an improvement from –34% last quarter, due to a more favorable product mix as well as beneficial impacts from digesting the fresh-start accounting inventory in the last quarter (following the firm’s emergence from Chapter 11 bankruptcy protection).

Operating expenses were $61m, reduced from $108m a year ago, since Wolfspeed has cut OpEx by $200m on an annualized basis.

“Operational performance continues to improve,” notes chief financial officer Gregor van Issum. “We are producing the same revenue with less capacity consumed. These continuous efforts position us to keep expanding our earnings potential per dollar of invested capital, even if it makes the reported under-utilization look larger.”

Net loss is up from $110.8m a year ago to $128.2m. However, this has been cut from $159.3m last quarter.

Operating cash flow was –$83.8m, cut from –$142.1m a year ago due to improvement in precious metal reclamation, interest income, and continued improvements in working capital. Net spending on property, plant and equipment (PPE) has been cut from $24.1m a year ago to just $5m, due to $38m in gross capital expenditure (CapEx, mostly from previous commitments) nearly offset by $33m of New York State incentive receipts tied to Mohawk Valley investments. Patent spending has reduced slightly from $1.5m a year ago to $1.2m. Free cash flow was therefore –$90m, cut from –$167.7m a year ago.

During the quarter, cash, cash equivalents and short-term investments fell from $1.292bn to $1.165bn.

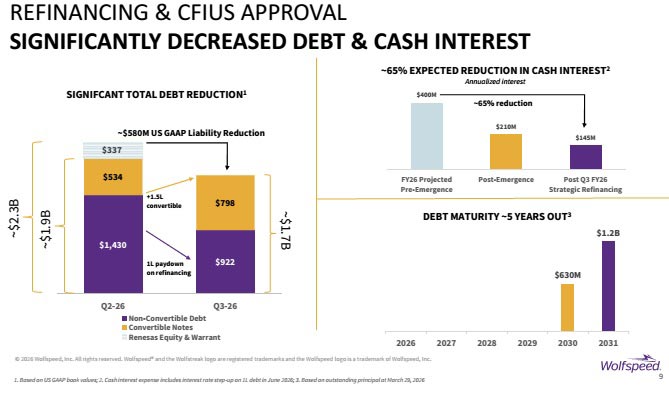

Capital restructuring reduces debt and interest expense

During the quarter, Wolfspeed took a “significant step” to strengthen its capital structure by raising $476m via: private placements of new convertible 1.5-lien senior secured notes, common stock, and pre-funded warrants. Using cash on hand to cover fees associated with the private placements, the gross proceeds were used to reduce the balance of existing highest-cost first-lien senior secured notes (for which the interest rate is 14%, and would step up further to 16%) by about 43%. This cut total debt by $97m, and should reduce annual interest expense by about €62m. “Our first debt maturity remains in 2030, providing runway to execute our strategic plans as we continue to optimize our capital structure,” says van Issum.

Also, Wolfspeed’s Chapter 11 bankruptcy protection procedures were completed after gaining clearance from the Committee on Foreign Investment in the United States (CFIUS) for the issuance of equity to Japan-based Renesas.

Due mainly to the strategic refinancing and reclassification of Renesas ownership, Wolfspeed’s equity has hence increased by more than $400m, significantly improving the debt-to-equity ratio.

Funding strategic priorities

“Backed by $1.2bn in liquidity and rigorous operational discipline, we are well-positioned to continue to fund our highest-priority initiatives,” says van Issum.

“We continued to make meaningful progress against our priorities, improving Wolfspeed’s long-term growth trajectory and our financial flexibility to execute our strategic priorities,” says Feurle. “We accelerated innovation across the business, launching our next-generation TOLT portfolio, introducing the first commercially available 10kV silicon carbide power MOSFET, and continuing to advance our 300mm substrate platform. At the same time, we continue to deepen our engagement with a diversified customer base,” he adds.

“Last quarter, we outlined the realignment of our go-to-market strategy around four verticals: Automotive, Industrial & Energy [I&E, including AI data centers and grid], Aerospace & Defense, and Materials,” notes Fuerle. “During the quarter [fiscal Q3], we have sharpened our approach with the completion of recent leadership additions, including Daihui Yu as regional president for Greater China, Stefan Steyerl, vice president of sales for EMEA, and most recently Yasuhisa Harita as regional president for Asia Pacific. These leaders strengthen our ability to scale our go-to-market efforts globally, and we are encouraged by the early traction we are seeing across each of these end-markets.”

In Auto, global EV adoption continues to grow, though more modestly in certain regions. “Silicon carbide revenue does not necessarily scale in lockstep with vehicle sales due to design-in and qualification cycles. As the industry evolves, we believed that we needed to retool the approach as the market entered its next phase. Therefore, we strengthened our team with experienced automotive executives and launched a focused strategy targeting key global accounts with high SiC adoption, positioning Wolfspeed to capture the next wave of design wins,” reckons Fuerle. “Given the qualification cycles of EV programs, our success from these engagements is expected to translate into revenue over time.”

In I&E, momentum in AI data-center applications continues to build. “Our TOLT portfolio is purpose-built for AI direct power, and we are actively collaborating with AI ecosystem partners on the transition from 400V to 800V architectures,” notes Fuerle.

In Aerospace & Defense, growth is supported by electrification trends and increasing demand for secure domestic supply chains. “In addition, we continue to expand our presence in emerging applications such as electric aviation. Our partnership with a leading manufacturer of electrical vertical takeoff and landing aircraft is a strong example of how our solutions enable higher efficiency and power density in next-generation platforms,” says Fuerle.

In our Materials business, we continue to serve our under-150mm materials customers, including under the long-term agreement (LTA) framework. In addition, we are making progress with qualification on 200mm material,” says Fuerle. “At the same time, we are engaging with AI ecosystem companies to explore how 300mm substrates can address thermal, mechanical and electrical challenges in next-generation AI high-performance computing packaging architectures. We continue to engage on 300mm as a longer-term opportunity.”

Growth in AI data centers and I&E applications to offset softness in EVs

For fiscal fourth-quarter 2026, Wolfspeed expects revenue of $140–160m. Gross margins is expected to remain negative. “Improving factory utilization remains one of the most important levers to drive margin expansion going forward,” stresses van Issum. Operating expenses should be approximately flat with fiscal Q3. “With headcount reduction actions largely complete, Wolfspeed expects to maintain approximately this level of OpEx,” he adds.

“In the long term, our objective remains clear: to return to above-market revenue growth driven by a more diversified customer base and to achieve EBITDA and cash flow profitability,” says van Issum.

“While near-term demand in automotive remains uncertain, we continue to see encouraging momentum in high-growth areas such as AI data centers and other I&E applications. These markets represent meaningful long-term opportunities, though it will take time for them to scale and offset current softness in automotive,” he notes.

Wolfspeed appoints executives to strengthen leadership team

Wolfspeed appoints Tokyo-based regional president for Asia Pacific

Wolfspeed appoints regional president, Greater China

Wolfspeed adds VP of sales for EMEA

CFIUS clears Wolfspeed issuance of equity to Renesas as part of court-approved restructuring

Wolfspeed produces single-crystal 300mm silicon carbide wafer

Wolfspeed cuts quarterly loss after CapEx slashed during restructuring

Wolfspeed’s quarterly revenue rebounds by 6%, led by 10% growth in Power Products