News: Microelectronics

16 February 2026

Wolfspeed’s soft demand for EV application offset by 50% quarterly revenue growth for AI data-center application

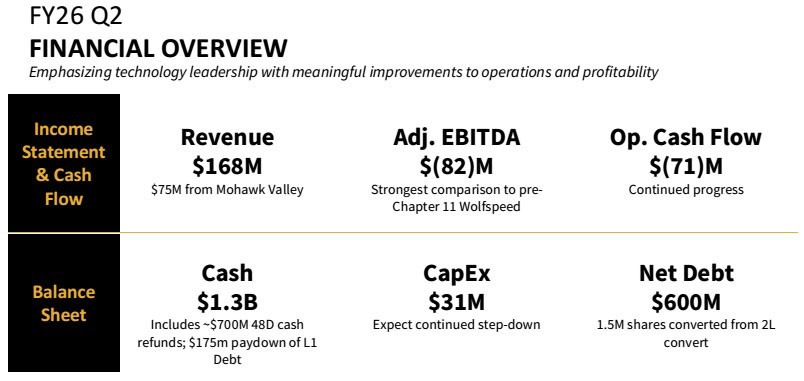

For its fiscal second-quarter 2026 (to end-December 2025), Wolfspeed Inc of Durham, NC, USA — which makes silicon carbide (SiC) materials and power semiconductor devices — has reported revenue of $168m, down 14.6% on $196.8m last quarter and 6.9% on $180.5m a year ago.

The drop followed accelerated customer purchases in fiscal Q1 (as certain customers built up inventory by placing orders from the 150mm-wafer Durham fab prior to its planned closure at year-end).

Also, certain customers pursuing second-sourcing of products during Wolfspeed’s bankruptcy process. After filing for Chapter 11 bankruptcy protection on 30 June, Wolfspeed emerged from Chapter 11 on 29 September.

In addition, in line with others in the industry, Wolfspeed has experienced ongoing softness in demand for applications including electric vehicles (EVs) that it expects will continue through fiscal 2026.

Materials Products revenue has fallen by 44% from $89.7m a year ago to $50.2m, driven largely by a tightening demand environment and increased competition in the market.

Power Products revenue has grown by 30% from $90.8m a year ago to $118.3m. This includes some of the last-time-buy shipments from the 150mm-wafer Durham fab ahead of its shutdown at the end of November, a month ahead of schedule. The 200mm-wafer Mohawk Valley Fab in Marcy, NY (opened in April 2022) contributed $76m, as the remaining production shifted from Durham.

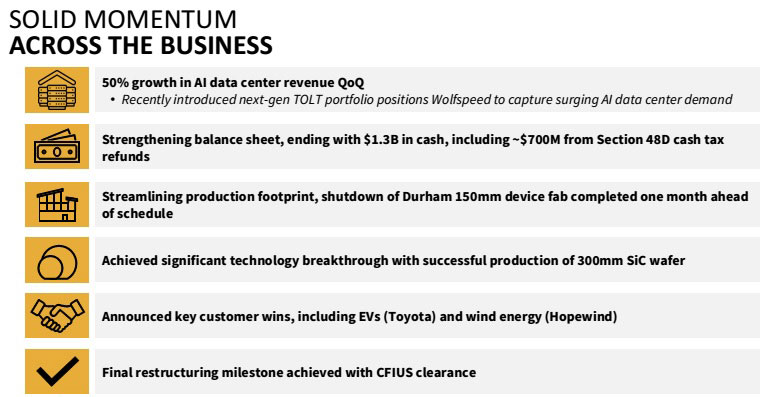

“The revenue tracking is a mix between a weaker automotive market and fast-growing mid- to high-voltage revenue. This is linked to the good traction in AI and data-center space,” notes chief financial officer Gregor van Issum. “We are also continuing to diversify our end-markets, particularly in mid- and high-voltage verticals like AI data centers, where we generated 50% sequential quarterly revenue growth [doubling over the last three quarters],” says CEO Robert Feurle. This reflects a “modest but expanding part of the firm’s business with meaningful long-term potential”.

On a non-GAAP basis, gross margin has gone from +2% a year ago and –26% last quarter to –34%. However, this was impacted by $39m in fresh-start accounting charges after emerging from bankruptcy ($23m of which is related to a one-time step-up in fair value of inventory, which was fully recognized within cost of revenue during the quarter), as well as a recurring $60m increase related to amortization for intangible assets, plus $14m of costs related to specific inventory reserves, and $48m of under-utilization costs. Closure of the Durham 150mm device fab at the end of November benefitted gross margins by $5m.

Net loss is up from $122.6m ($0.95 per diluted share) a year ago to $159.3m ($6.11 per diluted share).

Strengthening balance sheet

“During the quarter, we took decisive actions to strengthen our balance sheet,” notes van Issum. “First, we maximized the value of our [Section] 48D Advanced Manufacturing Tax Credit, receiving approximately $700m ahead of schedule. We used some of the proceeds to retire approximately $175m of outstanding [first lien] debt, an important step to reduce our leverage and interest expense. In addition, approximately 1.5 million shares have been converted from our second-lien convert, resulting in a debt reduction of approximately $18m. Together, this forms a first step to further improve our balance sheet post-emergence and will deliver $25m in annual interest savings.”

“Next, we drove strong working capital improvements [contributing about $89m, partially offset by final liability management payments of $64m] by proactively aligning production with the current demand environment, leading to a reduction in inventory and improving our receivables position,” continues van Issum.

“Lastly, we significantly improved operating cash flow performance [from –$195.1m a year ago to –$42.6m] by reducing operating expenses by $200m on an annualized basis [streamlining R&D to focus exclusively on high-return programs in the highest-growth markets] and capital expenditures by more than 90% compared to the same quarter last year [from about $400m to just $31m],” he adds. All capital expenditures were limited to previously committed investments.

After fresh-start accounting applied due to emergence from Chapter 11, Wolfspeed recorded a $1.1bn gain, which reflects about $3.7bn in debt forgiveness, offset by about $2.6bn of net adjustments to assets, primarily property, plant and equipment (PPE).

Overall, free cash flow improved from –$598.1m a year ago and $99.6m last quarter to +$627.1m.

During the quarter, cash, cash equivalents and short-term investments rose from $926m to $1.292bn, providing financial flexibility to execute on the firm’s self-funded business plan post-emergence.

Supported by improved liquidity measures and liability management payments of $64m, net debt at quarter-end was about $600m, with annual cash interest expense reduced by about 60%.

The reduction in property, plant and equipment (PP&E), partially offset by the step-up in intangibles, will result in a net reduction in ongoing depreciation & amortization expense of about $30m per quarter, which will be fully realized as inventory turns.

Business outlook

For its fiscal third-quarter 2026 (to end-March), Wolfspeed expects revenue to fall to $140–160m. The drop is due primarily to the accelerated customer purchases in fiscal first-half 2026 (building up inventory from the Durham fab prior to its closure at calendar year-end), certain customers pursuing second-sourcing of products during Wolfspeed’s bankruptcy process, and the ongoing weaker EV demand.

Driven by ongoing operational actions, gross margin should improve quarter-over-quarter, but remain negative. “We will continue to see benefits going forward as we focus on our 200mm device manufacturing in Mohawk Valley [as utilization increases, following closure of the 150mm Durham fab],” notes van Issum.

Operating expenses should be flat to slightly down sequentially, and $200m lower year-on-year, as management remains focused on controlling operating costs through actions that have already been implemented.

“We remain committed to a disciplined capital allocation strategy and driving CapEx further down over time as prior commitments start to fall off,” says van Issum.

“We are concentrating in a few key areas: strict financial discipline, advancing our technology leadership, and driving operational excellence,” says Feurle. “A central theme across these three priorities is diversifying our revenue base in key verticals where I believe we can extend our leadership position, particularly in mid- to high-voltage applications.” To accomplish this, Wolfspeed has broadened its go-to-market strategy by organizing it around four verticals that it believes will drive growth in our business in the near- to mid-term: automotive, industrial energy (including AI data centers and grid), aerospace & defense, and materials.

“Automotive remains a core market despite muted EV demand due to a mix of macro and structural factors, which include higher interest rates in the US and Europe, elimination of certain government incentives in the US, excess supply across the market, and intensifying competition globally, including China,” says Feurle. “While these headwinds are creating a softer demand environment in the near term, silicon carbide remains a foundational technology for EV and other platforms. Despite weaker near-term demand, our portfolio is aligned with OEMs that produce efficiency, range and power density. A great example of this is our recently announced partnership with Toyota to power the onboard charging systems for their battery electric vehicles. Thanks to the efforts of our leadership team that is strengthening our relationship with the top global EV OEMs, we are now sampling across several key strategic programs,” he adds.

“While the automotive end market remains volatile in the near term, we are encouraged by the growing momentum in key strategic areas such as AI data centers and other industrial and energy applications,” says van Issum.

“During Q2, we continue to fortify our sales, marketing, and product teams, adding experienced leaders with deep semiconductor knowledge and strong customer relationships,” says Fuerle. “These hires are already helping us extend our reach into emerging power device opportunities.” Key customer wins include Hopewind (to support its high-performance industrial and renewable energy inverters).

In particular, Wolfspeed’s recently introduced next-generation TOLT portfolio is expected to position the firm to capture surging AI data-center demand. “These emerging opportunities represent meaningful long-term growth drivers, but they will take time to scale and offset the continued softness in EVs,” cautions van Issum.

“While the near-term demand picture remains dynamic, two trends remain clear. First, electrification is happening across new markets every day. Second, voltages will continue to increase, necessitating more power density and increased energy efficiency,” notes Feurle.

“In materials, we demonstrated our capabilities in 300mm silicon carbide wafer production, a critical step towards entering emerging markets beyond power devices. One example is optical-grade silicon for next-generation AR/VR systems,” he adds.

“We now have the team and structure in place to navigate near-term demand dynamics and execute with discipline as we scale for long-term growth,” reckons Feurle.

“We are building a stronger, more resilient Wolfspeed. With an improved financial foundation, experienced leadership team, and our vertically integrated platform, we are strategically positioned to drive long-term growth and value,” Feurle concludes.

CFIUS clears Wolfspeed issuance of equity to Renesas as part of court-approved restructuring

Wolfspeed produces single-crystal 300mm silicon carbide wafer

Wolfspeed cuts quarterly loss after CapEx slashed during restructuring

Wolfspeed completes financial restructuring and emerges from Chapter 11 protection

Wolfspeed’s quarterly revenue rebounds by 6%, led by 10% growth in Power Products