News: Suppliers

7 November 2022

Aixtron shipment pushouts in Q3 to lead to record revenue in Q4

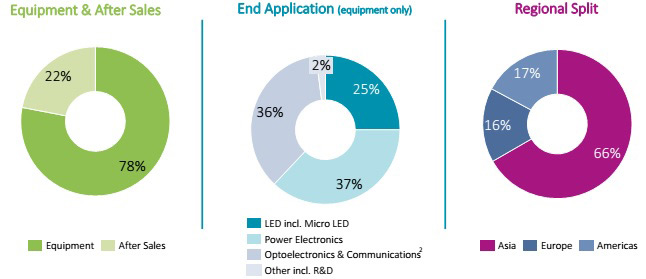

For the first nine months of the year, deposition equipment maker Aixtron SE of Herzogenrath, near Aachen, Germany has reported revenue growth of 13% year-on-year, from €248.1m in 2021 to €279.9m in 2022 (with 78% coming from equipment sales and 22% from after-sales service & spare parts).

Of the equipment revenue, metal-organic chemical vapor deposition (MOCVD)/chemical vapor deposition (CVD) equipment for making gallium nitride (GaN)- and silicon carbide (SiC)-based power electronics devices comprised 37% (with SiC growing strongly); MOCVD equipment for making optoelectronics devices (telecoms/datacoms and 3D sensing lasers for consumer electronics, solar, and wireless/RF communications) comprised 36% (with optical data transmission and 5G applications growing strongly); and MOCVD equipment for making LEDs comprised just 25% (mainly traditional red LEDs, but also micro-LED applications).

On a regional basis, 66% of revenue came from Asia (roughly the same year-on-year), 17% from the Americas (up from 10%), and just 16% from Europe (down from 23%).

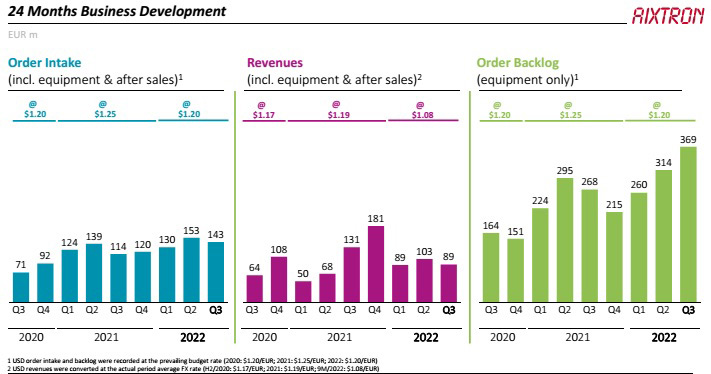

Third-quarter 2022 revenue was just €88.9m, down 13.3% on €102.5m in Q2/2022 and 32% on €130.8m a year ago. However, this was due mainly to a few customer-related delivery delays (shifting some tool deliveries into Q4/2022) and delays to the granting of export licenses. Over half of revenue came from equipment for manufacturing GaN and SiC power electronics. Sales of systems for manufacturing lasers (in particular for optical data transmission and 3D sensor technology) were also strong.

Gross margin for the first nine months of 2022 was 40%, down slightly year-on-year from 41%. However, Q3/2022 gross margin was 44%, up from 37% last quarter and 43% a year ago, due mainly to improved product mix.

Operating expenses have risen further, from €20.1m in Q3/2021 and €20.6m in Q2/2022 to €23.1m in Q3/2022, contributing to €65.4m in the first nine months of 2022 (up year-on-year from €60.3m), due to higher variable compensation components and lower R&D grants.

Operating profit (EBIT, earnings before interest and taxes) improved to €47.6m in the first nine months from €41.1m a year previously, with EBIT margin remaining 17% of revenue. However, Q3/2022 EBIT of €16.2m was down from Q2/2022’s €17.2m and Q3/2021’s €36.2m (with margin of 18% down from 28% a year ago).

Net profit in Q3/2022 was €19.1m (€0.28 per share, or 21% of revenue), down on €31.4m (€0.39 per share, 24% of revenue) a year ago. However, this is up on €17.3m (€0.16 per share, 17% of revenue) last quarter. Net profit for the first nine months of 2022 was €50.2m (€0.45 per share, 18% of revenue), up from €42.9m (€0.17 per share, 17% of revenue) a year ago.

Operating cash flow now positive

Operating cash flow has improved from -€27.6m in Q2/2022 to €0.5m in Q3/2022.

Capital expenditure (CapEx) has almost doubled from €4.2m in Q2/2022 to €8m in Q3/2022 (contributing to CapEx for the first nine months of the year rising from €13.3m for 2021 to €16.9m for 2022), largely investments in new-generation MOCVD tools.

Free cash flow was hence -€7.5m in Q3/2022, but this is a significant improvement on -€19m in Q3/2021 due to higher advance payments from customers. For the first nine months of 2022, free cash flow was €19m, due mainly to the high cash inflow from receivables.

Due to the push-out of shipments from Q3 and in preparation for the exceptionally high shipments expected in Q4/2022, inventories have risen to risen further, from €161.6m at the end of June to €209.2m at the end of September.

However, the increase in inventories was outweighed by a further rise in advance payments received for customer orders, from €103.7m at the end of June to €121.8m at the end of September (almost a third of the order backlog).

Overall, cash and cash equivalents (including financial assets) has fallen further, from €352.5m at the end of December and €346.2m at the end of June to €339.2m at the end of September, but this is due largely to the dividend payment of €33.7m agreed at the annual general meeting (AGM) of shareholders on 25 May (a payout ratio of 35% of the firm’s net income).

Aixtron says that its financial strength is underlined by its high equity ratio of 75% at the end of September. Meanwhile, staffing has risen to 842 at the end of September, up 9% from 772 at the end of June and 19% on 710 a year previously, so structural strengthening of the organization for further growth is reckoned to be well on track.

Q3 order intake up 25% year-on-year, driven by GaN- and SiC-based power electronics

Order intake in the first nine months of the year rose by about 13% year-on-year from €377.6m for 2021 to €425.6m in 2022, including €142.8m in Q3, up 25% on €114.2m in Q3/2021. This reflects “consistently high demand” for efficient GaN- and SiC-based power electronics (with the new-generation G10-SiC fully automated multi-wafer (9x6” or 6x8”) batch CVD system — launched just in mid-September — already comprising the single largest contribution in Q3, followed by GaN), as well as demand for lasers and LEDs (including micro-LEDs).

As of end-September, equipment order backlog was €369.4m, up 17.5% on €314.4m at the end of June and up 38% on €267.6m a year previously.

Due to the unabated strong demand and stable supply chains plus the shipment push-outs from Q3/2022, Aixtron expects exceptionally high shipments in Q4/ 2022, resulting in record quarterly revenue.

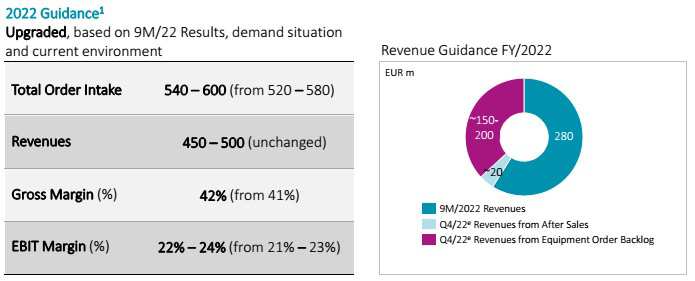

Full-year 2022 guidance upgraded

Based on a budget rate of $1.20/€ (versus $1.25/€ in 2021), in view of the continued improvement in demand, Aixtron has raised its guidance for full-year order intake from €520-580m to €540-600m.

Based on revenue in the first nine months of 2022 of €279.9m plus a forecasted €20m in after-sales spares & services revenue in Q4/2022, joined by equipment order backlog as of end-September of €150-200m (convertible into revenue during 2022), Aixtron still expects double-digit growth in full-year revenue to €450-500m in 2022.

However, in view of the improvement in product mix (for the remainder of 2022, compared with the first half), Aixtron has raised its guidance for gross margin from 41% to about 42% and for EBIT margin from 21-23% to 22-24%.

“The increase of our 2022 guidance in this challenging environment is the result of rising demand for our pioneering technologies,” comments chief financial officer Dr Christian Danninger. “Our strategic initiatives regarding product development and supply chain management are taking effect,” he adds.

“We are very pleased with the success of our recently launched G10-SiC and expect similar success for the upcoming launches of our new system generations,” says CEO & president Dr Felix Grawert. “The G10 silicon carbide is the first member of the new series family that we are launching. Also for GaN power electronics and for gallium arsenide lasers and micro-LED, we have new family members in the making. We are planning to launch both of them in first-half 2023. These products are in the validation at multiple beta customers,” he adds. “The increasing share of fully automated systems also shows the strong demand for new technologies.”

“Overall, the current global crisis situations and market developments continue to have only a minor impact on business,” notes Aixtron. “Logistics and supply chains are tense, but in our view remain stable overall.”

Aixtron launches G10-SiC 200mm CVD system

Aixtron’s Q2 revenue up 51% year-on-year, driven by demand from SiC and GaN power electronics

Aixtron expands MOCVD market share to 75% in 2021

Aixtron grows revenue 59% and orders 65% in 2021, driven by power electronics