News: Suppliers

4 May 2026

Aixtron’s Q1 revenue down 47% year-on-year, but opto drives 30% growth in orders

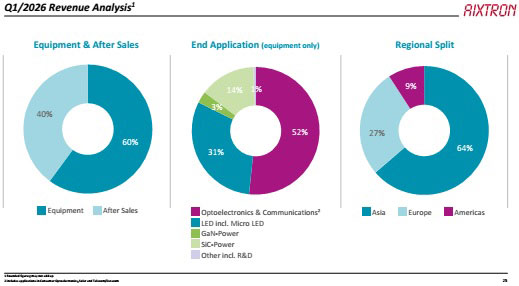

Confirming its preliminary figures released on 14 April, for first-quarter 2026 deposition equipment maker Aixtron SE of Herzogenrath, near Aachen, Germany has reported revenue of €59.4m, down 47% on €112.5m a year ago and down 68% on €187m last quarter, but within the guidance of €65m±€10m. Of total revenue, as much as 40% came from after-sales, and only 60% from equipment sales (€35.7m, down 52% on €87.7m, or 78% of total revenue, a year ago).

Of total equipment revenue, power electronics applications contributed 17% (plummeting from 69% a year ago). Specifically, demand for silicon carbide (SiC) chemical vapor deposition (CVD) tools remained soft, at 14% of equipment revenue, reflecting ongoing customer under-utilization. Demand for gallium nitride (GaN) metal-organic chemical vapor deposition (MOCVD) tools remained stable, at a low level of 3%.

MOCVD equipment for making LEDs comprised 31% of equipment revenue (up from 17% a year ago).

MOCVD equipment for making optoelectronics devices (telecoms/datacoms and 3D sensing lasers for consumer electronics, solar, and wireless/RF communications) has boomed from just 10% of equipment revenue a year ago to 52% in Q1/2026.

On a regional basis for first-quarter 2026 revenue, 27% from Europe (up from just 15% a year ago), while 64% came from Asia (down from 70%) and just 9% from the Americas (down from 15%).

Margins and profits hit by one-off staff-cut expenses

Gross margin was 18% (down on 46% last quarter and 30% a year ago). However, this includes one-off expenses in the mid-single-digit-million Euro range related to the announced personnel reduction in the operations area, which is intended to create a more flexible operating structure.

Operating expenses have risen by 7% from €30.8m a year ago to €33m in Q1/2026, as R&D expenses were increased by 40% from €17.7m to €24.8m.

The operating result (EBIT) was –€22.3m (EBIT margin of –38%), compared with €58m (31% margin) last quarter and €3.3m (3% margin) a year ago, due mainly to the lower volume and to expenses for the one-off effects.

Net profit was –€21.9m (–€0.19 per share), compared with €47.9m (€0.42 per share) last quarter and €5.1m (€0.04 per share) a year ago.

Positive free cash flow

Aided in particular by a €76.3m reduction in working capital to €263.6m, operating cash flow was €53.6m (up from €35.1m a year ago). Capital expenditure was fairly stable year-on-year, at €5.1m. Free cash flow was hence €48.5m (up from €29.8m a year ago).

During Q1, cash and cash equivalents (including other current financial assets) therefore rose by €48.1m from €224.6m to €272.7m (up from €153.4m a year previously).

Aixtron notes that its equity ratio of 85% at end-March 2026 underscores its financial strength.

Strategic flexibility

In April, Aixtron placed a €450m convertible bond, further enhancing long-term financial flexibility. The zero-coupon bonds do not bear periodic interest and (unless converted before then) will be redeemed in April 2031.

“The successful placement of Aixtron’s first convertible bond underscores the capital markets’ confidence in the strength and long-term potential of our strategy,” says chief financial officer Dr Christian Danninger. “This now gives us full flexibility to act on future business opportunities,” he adds.

During Q1/2026, Aixtron announced plans for a new production site in Malaysia to strengthen long-term manufacturing flexibility and resilience, particularly in supporting customers in Asia.

“At the same time, we will remain financially disciplined and continue further optimizing working capital,” says Danninger.

Order intake and backlog

Signaling a “clear improvement in market momentum”, order intake in first-quarter 2026 was €171.4m, up slightly on €169.6m last quarter and up 30% on €132.2m a year ago, driven by very strong demand for optoelectronics systems (€118m, comprising almost 70% of order intake), underscored by multi-tool orders from several customers. “Laser-related demand exceeded our expectations,” says CEO Dr Felix Grawert.

As of end-March 2026, equipment order backlog was €359.1m, up 17% on €307.9m a year earlier and up on €257.8m at the end of 2025.

Updated 2026 full-year guidance confirmed

Supported by the healthy optoelectronics pipeline, for second-quarter 2026 Aixtron expects revenue to almost double to €110m±€10m, as major system shipments are expected to begin in Q2 and continue well beyond the current fiscal year.

In addition, GaN tool demand is expected to pick up later in 2026 due to higher customer utilization. SiC tool demand recovery is expected in second-half 2026 or early 2027.

“The visibility provided by orders extending beyond 2026 supports the start of a new structural growth trend,” says Grawert.

As Aixtron expects this momentum to continue, on 14 April it raised its full-year 2026 guidance for revenue from €520m±€30m to €560m±€30m, and for gross margin from 41–42% to about 42%, and EBIT margin from 16–19% to 17–20%. This includes one-off expenses in the mid-single-digit million Euro range related to the personnel reduction undertaken in the operations area.

Aixtron says that it continues to see high multi-tool order activity, contributing to a robust pipeline well beyond 2026. “The planned Malaysia site strengthens our foundation for profitable growth,” says Grawert.

Aixtron’s preliminary Q1 order intake up 30% year-on-year, driven by Opto comprising 65% share

Aixtron to build new manufacturing plant in Malaysia

Aixtron’s Q3 revenue and margin impacted by volume shifts into Q4

Aixtron’s revenue grows 22% in Q2, driven by AI data-center communications