News: Suppliers

20 March 2026

Veeco’s revenue down 9.4% year-on-year for Q42025 and 7% for full-year

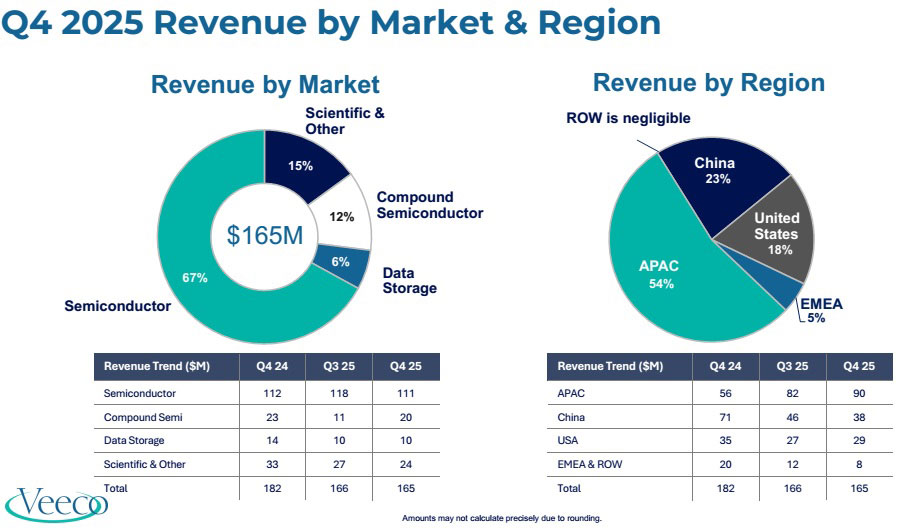

For fourth-quarter 2025, epitaxial deposition and process equipment maker Veeco Instruments Inc of Plainview, NY, USA has reported revenue of $165m, down 9.4% on $182.1m a year ago but roughly flat on Q3/2025’s $165.9m.

The Semiconductor segment (Front-End and Back-End, as well as EUV Mask Blank systems and Advanced Packaging) fell from $118.3m (71% of total revenue) last quarter to $110.5m (67% of revenue), although this is down only slightly on $112.1m a year ago.

The Compound Semiconductor segment (Power Electronics, RF Filter & Device applications, and Photonics including specialty, mini- and micro-LEDs, VCSELs, laser diodes) is down on $22.8m a year ago to $20.1m (12% of revenue). However, this is almost doubled last quarter’s $10.9m (7% of revenue).

The Data Storage segment (equipment for thin-film magnetic head manufacturing) was $10.2m (6% of revenue), down from $14.1m (8% of revenue) a year ago but up slightly on $10m last quarter.

The Scientific & Other segment (research institutions and other applications) has fallen further, from $33m (18% of revenue) a year ago and $26.7m (16% of revenue) last quarter to $24.2m (15% of revenue).

By region, Asia-Pacific (excluding China) has risen further (from 31% of total revenue a year ago and 49% last quarter to 54%), due to an increase in semiconductor sales (mainly in Taiwan). Conversely, there was shrinkage for China (from 39% then 28% to 23%) and Europe, Middle-East & Africa (EMEA) & the Rest of the World (from 11% then 7% to 5%). The USA rebounded slightly from 16% last quarter to 18% (almost level with 19% a year ago).

Full-year 2025 revenue down 7%

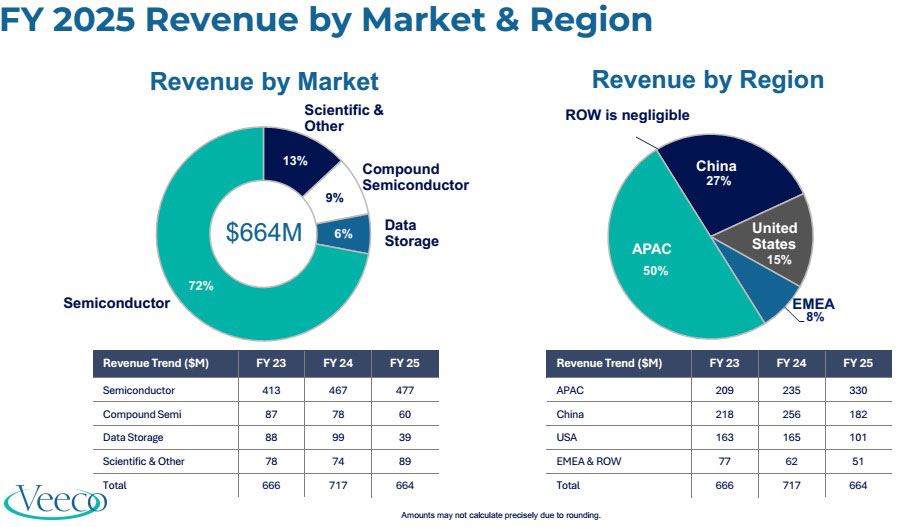

Full-year revenue fell by 7% from $717.3m in 2024 to $664.3m for 2025.

The Semiconductor segment grew by 2% from a record $466.6m (65% of total revenue) in 2024 to another record of $476.7m (72% of revenue) in 2025, driven mainly by laser annealing and ion beam technology, as well as wet processing and lithography tool shipments for advanced packaging (which doubled from $75m in 2024 to $150m in 2025, driven by AI-related demand).

The Compound Semiconductor segment fell by 23% from $77.6m (11% of revenue) in 2024 to $59.6m (9% of revenue) in 2025.

The Data Storage segment more than halved from $98.9m (14% of revenue) in 2024 to $39.2m (6% of revenue) in 2025.

The Scientific & Other segment rose by 20% from $74.2m (10% of revenue) in 2024 to $88.9m (13% of revenue) in 2025, including some large quantum computing orders.

By region, the Asia-Pacific (excluding China) rose further, from 32% of revenue in 2024 to 50% in 2025, led by shipments to a leading Taiwanese semiconductor customer for multiple Veeco products. Conversely, there was shrinkage for China (from 36% to 27%, with a decline in laser annealing systems), the USA (from 23% to 15%), and EMEA and the Rest of the World (from 9% to 8%).

Profit margins reduced by product mix shifting towards advanced packaging

On a non-GAAP basis, full-year gross margin fell from 43.3% in 2024 to 41% for 2025. Quarterly gross margin was 37.7%, down on 41.9% last quarter and 41.5% a year ago, due to product mix shifting more towards lower-margin advanced packaging, plus some impact from sign-offs from evaluation systems.

Operating expenses were $48.5m, up on $46.3m last quarter and $48.1m a year ago. Nevertheless, full-year operating expenses have been cut from $194.4m in 2024 to $188m in 2025.

Operating income has fallen further, roughly halving from $27.4m a year ago and down from $23.1m last quarter to $13.8m. Full-year operating income hence fell from $116.1m in 2024 to $84.3m for 2025.

Net income has fallen further, from $24.2m ($0.41 per diluted share) a year ago and $21.8m ($0.36 per diluted share) last quarter to $14.7m ($0.24 per diluted share). Full-year net income hence declined from $104.3m ($1.74 per diluted share) in 2024 to $80.2m ($1.33 per diluted share) for 2025.

Cash flow from operations was $25m, bringing the total for 2025 to $69m (up on 2024’s $64m). Capital expenditure (CapEx) was $3m for Q4 and $16m for full-year 2025. During Q4/2025, cash and short-term investments hence rose by $21m, from $369m to $390m. Long-term debt remains $226m.

From a working capital perspective, accounts receivable fell by $5m to $111m. Inventory grew by $12m to $275m. Accounts payable rose by $11m to $55m. Customer deposits included within contract liabilities on the balance sheet grew by $14m to $50m.

Order backlog grows by 35% in 2025

Order backlog has grown by 35% from $410m at end-2024 to $555m at end-2025. “Veeco executed well in 2025, accelerating bookings in the second half for our semiconductor, compound semiconductor and data storage markets, positioning us for robust growth in 2026 [principally in second-half 2026] driven by AI and high-performance computing,” says CEO Bill Miller Ph.D.

“With expanding backlog, growing customer adoption of our new technologies, and the planned merger with Axcelis, we believe we are well positioned to accelerate growth and create long-term strategic value for all stakeholders,” says Miller.

At a Special Meeting on 6 February, Veeco’s stockholders voted to approve all proposals related to its pending merger with ion implantation system maker Axcelis Technologies Inc of Beverly, MA, USA, which is expected to be completed in second-half 2026.

Guidance and outlook

For first-quarter 2026, Veeco expects revenue of $150–170m. Gross margin should be 37–38%. With OpEx of $48–50m, the firm expects operating income of $9–16m and net income of $9–15m ($0.14–0.24 per diluted share).

For the full year, Veeco expects revenue to grow by about 16% from 2025’s $664.3m to $740–800m for 2026.

After strong growth in 2025, Scientific & Other revenue is expected to fall by about 33% to $60m. However, Semiconductor revenue should grow by 15% to $550m (in line with forecasted wafer fabrication equipment market growth of 10–20%), Compound Semiconductor revenue is expected to grow by about a third to $80m, and Data Storage revenue should double to about $80m.

“With the semiconductor market, we expect strong growth from our tier-1 customers [at the leading edge], driven by AI and high-performance computing, more than offsetting declines in mature-node China business. We are seeing accelerating demand for our LSA [laser spike annealing] tools at advanced nodes, along with growth in wet processing applications for advanced packaging as customers scale capacity driven by AI and HBM [high-bandwidth memory],” says senior VP & chief financial officer John Kiernan.

“In the compound semiconductor market, we see growth in 2026, weighted in the second half. We received several orders in 2025 for our new Propel 300mm GaN-on-silicon [metal-organic chemical vapor deposition (MOCVD)] system for GaN power [including a pilot line worth $15m shipping in 2026, with further orders possible in second-half 2026 for shipment in 2027] and micro-LED applications [with a tool in backlog], as well as orders for our new Lumina+ arsenide-phosphide [MOCVD] system, supporting photonics and solar end-markets. These new product wins are driving revenue in the second half of 2026 [and driving market share gains]. We’re also seeing continued engagement from customers and are taking orders for deliveries into 2027,” he adds. “We’re actually doing demos with a few different customers for micro-LEDs, as well as other GaN power opportunities.”

“In the data storage market, we see customers expanding capacity, increasing CapEx spend, and adopting heat-assisted magnetic recording [HAMR], resulting in increased orders in the third and fourth quarter of 2025 for our ion beam and wet processing equipment. This is driving an increase to revenue, principally in the second half of 2026,” says Kiernan. “These trends by our customers are driving momentum for our business as we are fully booked in 2026 and have multiple orders extending into 2027.”

For full-year 2026, gross margin should be 41–43%, with some acceleration in the second half of the year (up to Veeco’s targeted 45%) due to higher-margin new products, boosted by significantly higher volumes in the Data Storage business. Despite OpEx rising to $205–220m, Veeco expected growth is operating income to $101–126m and net income to $94–115m ($1.50–1.85 per diluted share).

“AI is a critical driver of Veeco’s growth in semi, compound semi, and data storage markets, and we have a strong portfolio of enabling technologies that are increasingly critical to serve leading customers,” reckons Kiernan. “From a semiconductor market perspective, analysts are projecting the industry to grow to over $1 trillion in the near term, with AI accounting for more than half of sales. We are confident that Veeco is well-positioned to create long-term value in an increasingly AI-driven semiconductor market.”

Veeco books multi-system Lumina and Spector orders for InP datacom laser manufacturing

Veeco stockholders approve merger with Axcelis

Veeco receives Propel300 MOCVD system order from GaN-on-Si power semiconductor IDM