News: Markets

14 July 2026

Smartphone market falls 4% year-on-year in Q2, driven by memory shortage

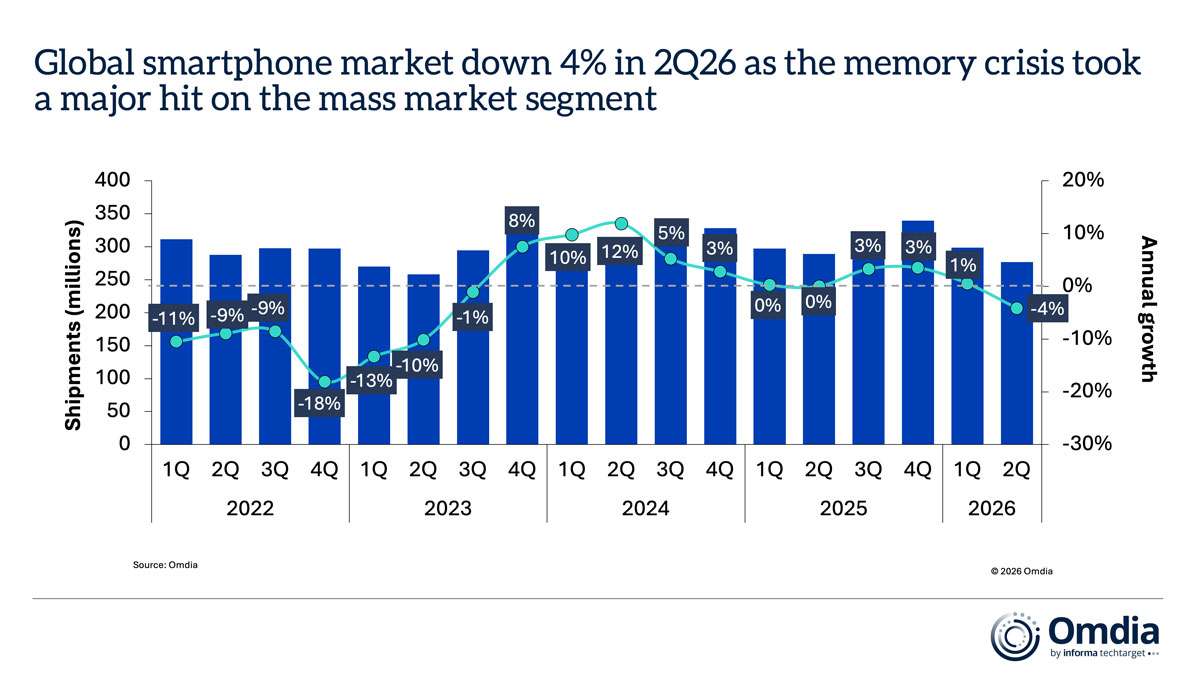

Global smartphone shipments fell 4% year-on-year in second-quarter 2026 as the ongoing memory crisis disrupted supply and pushed up component costs, according to Omdia’s Smartphone Horizon Service for July 2026 (sell-in shipments). The current dynamic has created severe market polarization, reflecting stark differences in vendors’ mitigation strategies, which vary according to their priorities, scale, price-band focus, and core audience demographics, notes the market research firm.

Graphic: Global smartphone market down 4% in Q2/2026.

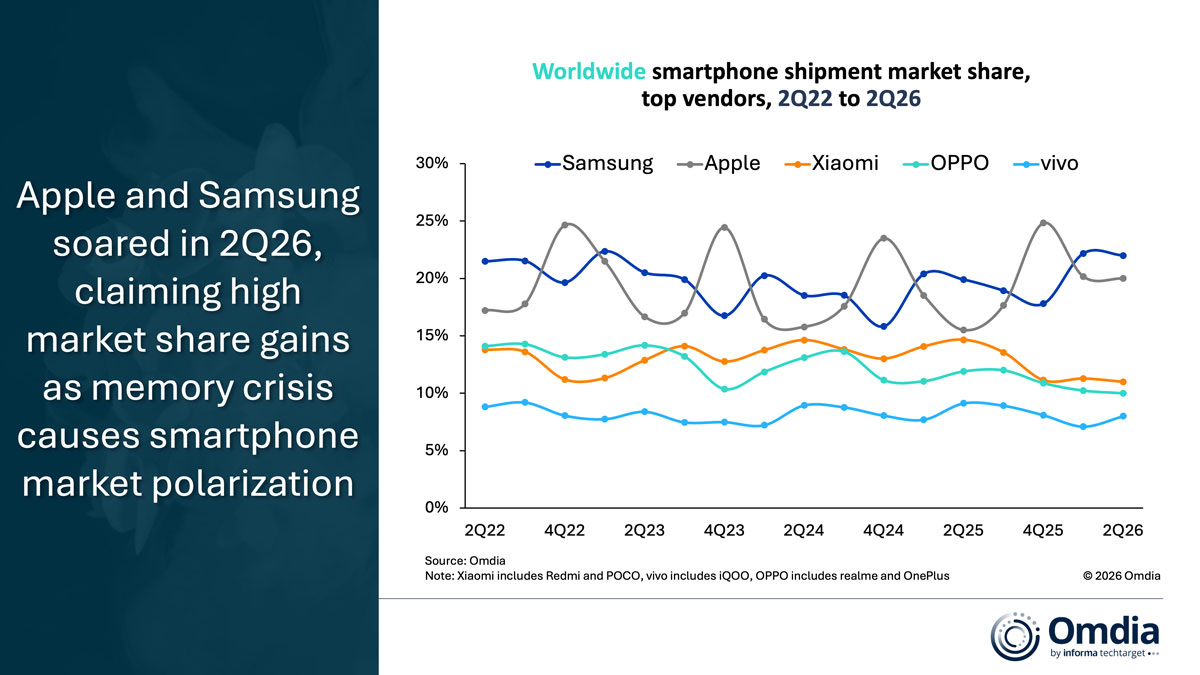

In particular, Samsung and Apple bucked the downward trend, growing shipments and increasing their market share by 2 and 4 percentage points compared with Q2/2025, respectively.

Samsung remained the largest smartphone vendor in Q2/2026 with 22% market share (up from 20% a year ago), helped by resilient demand and strong supply availability. The delayed launch of the Galaxy S26-series pushed some demand into the second quarter for the premium segment. At the same time, Samsung gained ground in the budget segment as Chinese rivals pivoted to a more conservative strategy, by reducing product lines and increasing device sell-in prices.

Apple delivered its best second-quarter performance ever, capturing a record-high 20% market share (up from 16% a year ago) during what traditionally is its slowest quarter of the year. The iPhone 17 series delivered one of the strongest iPhone refresh and upgrade cycles in Apple’s history. Apple also benefited from stable pricing while most competitors were forced to raise their pricing. However, as Apple raised pricing across other products towards the end of Q2, a key question remains to what extent iPhones might be impacted by similar hikes later this year.

Graphic: Worldwide smartphone shipment market share top vendors Q2/2022 to Q2/2026.

Meanwhile, mass-market segment declines squeezed many players beyond the top two. By rank, Xiaomi defended its third spot with 11% market share (down from 15% a year ago). OPPO held fourth at 10% share (down from 12%) as it underwent restructuring to optimize its three-brand umbrella. vivo rounded out the top five with 8% market share (deon from 9%).

“The steepest volume drops hit the sub-$400 mass-market segment, where supply constraints are tightest, profit margins are slimmest, and price sensitivity is highest,” says principal analyst Runar Bjorhovde. “To adapt, vendors are shifting their strategies from volume to value by reoptimizing portfolios and adjusting retail pricing. Managing the surging component costs is incredibly complex and unpredictable, with some vendors facing memory costing more than four to five times what they did a year ago. Memory and storage alone now account for more than 60% of the bill-of-material for budget devices and more than 30% for high-end models. Although memory and storage costs are the biggest challenges for vendors, they are far from the only challenge. New semiconductor bottlenecks, such as within foundries, are adding further cost pressures,” he adds.

“While vendors hope for near-term price corrections, memory price declines are expected to begin at the earliest in the second half of 2027. However, prices are unlikely to return to pre-2025 levels,” says research manager Le Xuan Chiew. “Smartphone vendors’ tactical adjustments should not be considered short-term response tactics but rather key permanent strategic shifts that will ensure business agility and sustainability in the years to come,” he adds.

“We anticipate the sharpest volume declines to hit in the upcoming two quarters, where normal seasonal demand peaks — driven by new launches, holidays and shopping festivals — collide with constrained memory chip supply,” says Bjorhovde. “Consequently, vendors are expected to lean further into the higher-price segments to capitalize on customers seeking device upgrades in 2026’s sales season. However, while moving upmarket protects margins and revenue, vendors offer fewer options to budget-constrained consumers. Many mass-market buyers will be forced to delay purchases, downgrade expectations, utilize financing, or opt for refurbished devices.”

Smartphone shipments grow 1% year-on-year in Q1 to 298.5 million units

Smartphone shipments to fall 7% in 2026 amid memory constraints and geopolitical pressures