29 May 2025

Micro-LED display chip market growing at 93% CAGR to US$744.7m in 2029

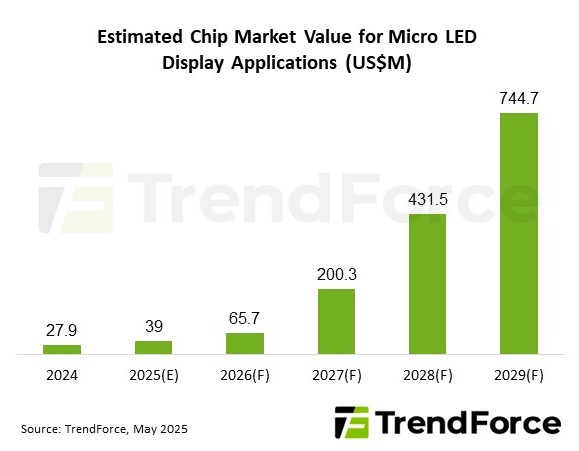

The chip market for micro-LED display applications is rising at a compound annual growth rate (CAGR) of 93% from US$27.9m in 2024 and US$39m in 2025 to US$744.7m by 2029, forecasts TrendForce.

The market research firm’s latest report ‘2025 Micro LED Display and Non-Display Application Market Analysis’ shows that current development of micro-LED technology in the display sector focuses on two key challenges: optimizing manufacturing costs through design and production improvements, and identifying unique niche markets.

Cost improvements continue for large-sized displays

Presently, the bulk of the display-related micro-LED market is driven by large-sized displays, where Samsung holds a leading position. Future growth will rely not only on breakthroughs across several critical manufacturing processes but also on collaborations between Chinese chipmakers and brand manufacturers to push chip miniaturization. This will further enhance cost advantages for mass-produced micro-LED large-sized displays, says TrendForce.

Additionally, as artificial intelligence (AI) broadens the application scenarios for head-mounted devices and as smart driving ecosystems drive up demand for advanced automotive displays, these two sectors are expected to become major pillars of the micro-LED display market in the years ahead.

TrendForce notes that the industry standard for micro-LED large-sized displays is typically 4K resolution or higher. However, the currently commercialized, mass-producible pixel pitch remains at 0.5mm. Continued efforts to reduce pixel pitch are essential to further differentiate micro-LED from mini-LED video walls, along with overcoming challenges like low yield rates in driver connections and issues with panel seams.

Cost optimization is also shifting toward the backplane, where simplifying the manufacturing process can improve yields, and reducing the number of seams can cut down assembly steps. This contributes to overall cost reductions.

Transparent displays hold great promise; non-display applications open new doors

Micro-LED technology also shows strong potential in transparent display applications. These can be categorized into direct-view and micro-projection systems, with the key differences lying in viewing angles and focal distance management. In terms of use case, transparent direct-view displays are better suited for public environments where multiple people view content, and the combination of high brightness and high transparency makes micro-LED technology ideal, says TrendForce.

Meanwhile, micro-projection systems hold greater promise in privacy-sensitive personal electronic devices, where micro-LED technology offers ultra-miniaturized light engine solutions and is seen as the best option for micro-display technology in augmented-reality (AR) applications. Overall, micro-LED technology has significant room for expansion across diverse transparent display segments by developing both TFT and CMOS backplane platforms.

TrendForce emphasizes that the immediate priority for the micro-LED industry is to scale up the market quickly in order to realize economic efficiencies. As a result, non-display sectors have increasingly become important avenues for growth in addition to focusing on display applications.

These non-display opportunities span a wide range, including optical communication applications accelerated by AI, biotechnology-related medical uses, and industrial production areas such as 3D printing and photopolymerization. Ongoing innovations in these areas are adding further momentum to micro-LED market expansion.

Micro-LED chip market to grow from $38.8m in 2024 to $489.5m by 2028

Micro-LED chip market growing at 84% CAGR to $579m by 2028

Micro-LED chip market to almost double to $27m in 2023, driven by large displays and wearables