News: Suppliers

8 August 2025

Veeco’s Q2 revenue, operating income and EPS exceed guidance, but constrained by tariffs

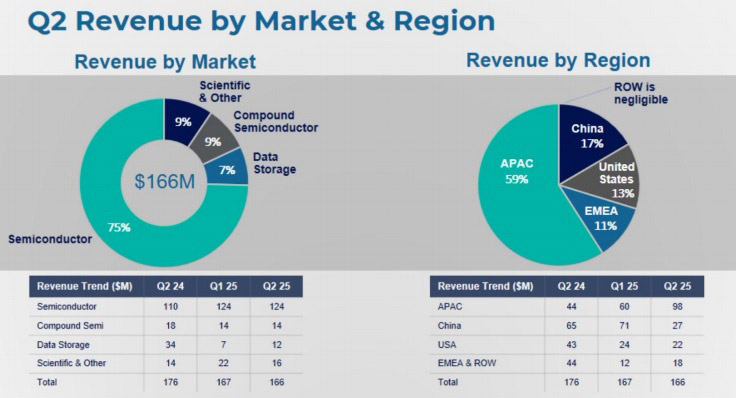

For second-quarter 2025, epitaxial deposition and process equipment maker Veeco Instruments Inc of Plainview, NY, USA has reported revenue of $166.1m, down slightly on $167.3m last quarter and 6% on $175.9m a year ago, but exceeding the $135–165m guidance.

“In our guidance for the quarter, we took into consideration the then imposed substantial import tariffs in China for goods manufactured in the USA. We reported certain China customers were delaying shipments due to the tariffs, and the midpoint of our guidance range assumed $15m of shipments would be delayed outside the quarter,” says chief financial officer John Kiernan. “During the second quarter, as the tariff rate was significantly reduced, customers accepted the majority of shipments that were previously delayed,” he adds. “The delay in tariff shipments was a one-time thing in Q2 that right now has been totally resolved.”

By region, China still plunged from $71m in Q1 to just $27m in Q2 (shrinking from 42% to 17% of total revenue). The Asia Pacific (excluding China) has grown further, from just $44m (25% of total revenue) a year ago to $60m (36% of revenue) in Q1 and now $98m (59% of revenue) in Q2, led by sales in Taiwan and Southeast Asia for advanced packaging as well as ion beam deposition for EUV mask blanks. The USA has almost halved from $43m (24% of revenue) a year ago to $24m (15% of revenue) in Q1 and $22m (13% of revenue) in Q2. Europe, Middle-East & Africa (EMEA) and the rest of the world (RoW) has rebounded from just $12m (7% of revenue) in Q1 to $18m in Q2 (11% of revenue), although this is still down on $44m (14% of revenue) a year ago.

Revenue growth has been fueled by rapid expansion of high-performance computing and AI technologies:

- The Semiconductor segment (Front-End and Back-End, as well as EUV Mask Blank systems and Advanced Packaging) contributed $123.9m (representing 75% of total revenue), flat sequentially but up 13% on $109.9m (63% of total revenue) a year ago. Growth is led by strong performance for wet processing and lithography systems for advanced packaging applications (driven by growing demand from AI by a broad base of customers, including leading foundries and OSATs) and ion beam deposition systems for EUV mask blanks applications, together with continued demand for laser spike annealing systems (with shipments to leading customers supporting gate-all-around and high-bandwidth memory applications).

- The Compound Semiconductor segment (Power Electronics, RF Filter & Device applications, and Photonics including specialty, mini- and micro-LEDs, VCSELs, laser diodes) contributed $14.2m (9% of total revenue), down on $18.2m (10% of total revenue) a year ago but level with last quarter.

- The Data Storage segment (equipment for thin-film magnetic head manufacturing) contributed $12.4m (7% of revenue), down on $34m (19% of total revenue) a year ago but almost doubling from just $6.7m last quarter.

- The Scientific & Other segment (research institutions and other applications) contributed $15.7m (9% of revenue), down from $22.4m last quarter but up on $13.8m (8% of revenue) a year ago.

On a non-GAAP basis, gross margin was 42.6%, down on 43.7% a year ago but up from 41.7% last quarter, and exceeding the expected 40–42%, favorably impacted by higher volume and improved product mix but impacted by about 100 basis points from tariffs.

Operating expenses were $47.6m, up on $45.5m last quarter but cut from $48.6m a year ago.

Net income has fallen further, from $25.4m ($0.42 per diluted share) a year ago and $22.2m ($0.37 per diluted share) last quarter to $21.5m ($0.36 per diluted share), but exceeding the guidance of $7–20m ($0.12–0.32 per diluted share).

Operating cash flow was $9m. Capital expenditure was $3m. During the quarter, cash & short-term investments rose hence from $353m to $355m, up on $305m a year ago.

Strengthening the balance sheet, Veeco retired all $25m of its convertible senior notes due in 2027, issuing 1.6 million shares of common stock and $5m of cash. Long-term debt has been cut from $250m to $225m.

Also during the quarter, Veeco entered into an amendment to its revolving credit facility, increasing the size from $225m to $250m and extending the maturity to June 2030.

“Both of these actions provide greater financial flexibility and liquidity as we focus on our key growth drivers for the business,” says Kiernan.

September-quarter guidance and outlook

For third-quarter 2025, Veeco expects revenue of $150-170m. Gross margin should be 40–42%, which assumes an impact of 100 basis points from tariffs.

“We’ve seen increased costs from tariffs on imported materials,” says Kiernan. “That said, we are actively working with our global supply chain partners to mitigate these impacts. Our teams are focused on cost containment, sourcing flexibility and operational efficiency to help offset potential headwinds.”

With operating expenses rising to $48–49m, net income is expected to drop slightly to $12–21m ($0.20–0.35 per diluted share).

“In the Semiconductor market, we continue to see growth potential in 2025, particularly in leading-edge investments driven by AI and high-performance computing. These trends are expected to support significant demand with growth in gate-all-around and advanced packaging technologies,” says Kiernan. “Beyond 2025, our outlook remains strong, supported by our differentiated product portfolio across laser annealing, ion beam deposition, wet processing and lithography,” he adds.

“While we expect revenue in the Compound Semiconductor market to decline in 2025 compared to 2024, we are seeing encouraging signs of growth for applications in GaN power, solar and photonics. These emerging opportunities are expected to begin contributing to revenue growth in 2026,” says Kiernan.

“Over the last few years in MOCVD, in particular, we've had a concerted effort to upgrade our product lines, specifically in 300mm GaN-on-silicon and in the batch arsenide-phosphide tools,” says CEO Bill Miller.

“The 300mm GaN-on-silicon [MOCVD] evaluation system we have in the field is progressing well. We’re competitive from a productivity and cost-of-ownership standpoint while maintaining excellent process performance, meeting the customer’s specification. Assuming success, the plan would be to have this drive pilot-line business for us starting in 2026… then ramping to high volume in 2027 and beyond,” he adds.

“In the arsenide-phosphide tool-set, we're working with a number of customers, for example, in low-earth-orbit solar activity. There’s some opportunities there: micro-LED and indium phosphide applications in the data center. So we’re working with a number of customers, and some of the feedback we’re receiving is that we’re really differentiated on performance with a lower cost of ownership for our customers.”

“In the Data Storage market, system revenue is declining year-over-year. However, our service revenue has increased, reflecting higher customer utilization. While it is too early to predict customer capacity additions for 2026, we are encouraged by increased engagement and commercial discussions around future requirements,” he adds.

“We continue to see strong demand in the Scientific market for our research-driven applications, particularly in quantum computing. This segment is expected to deliver growth in 2025, supported by ongoing investment in advanced scientific innovation,” Kiernan concludes.

Veeco announces private exchanges and cancels remaining 3.75% convertible notes due 2027

Veeco’s Q4 revenue and income exceed midpoints of guidance

Veeco’s record laser annealing sales compensate for declining compound semi revenue in Q2