News: Optoelectronics

22 August 2025

Lumentum’s June-quarter revenue and EPS exceed raised guidance

For its fiscal full-year 2025 (ended 28 June), Lumentum Holdings Inc of San Jose, CA, USA (which designs and makes optical and photonic products for optical networks and lasers for industrial and consumer markets) has reported revenue of $1645m, up 21% on $1359.2m in fiscal 2024.

Specifically, Cloud & Networking segment revenue rose by 30% from $1084.9m to $1410.8m. Industrial Tech segment revenue fell by 14.6% from $274.3m to $234.2m.

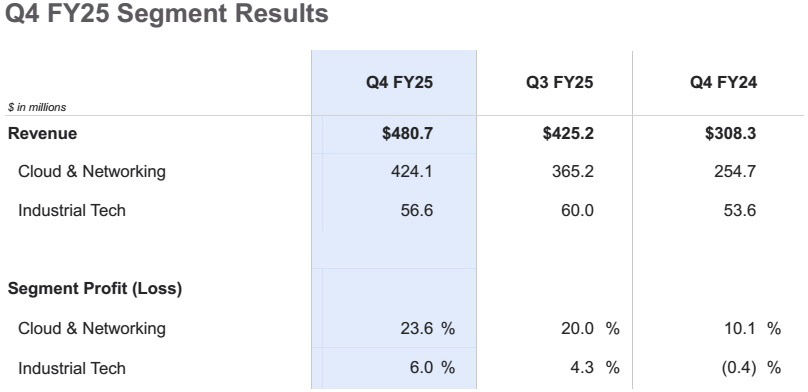

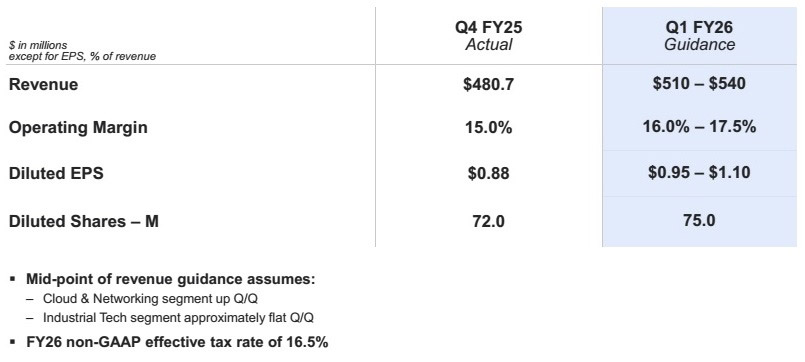

Fiscal fourth-quarter 2025 revenue was $480.7m, up 13.1% on $425.2m last quarter and 55.9% on $308.3m a year ago. This exceeds early June’s raised guidance range of $440–470m.

“We executed exceptionally well in meeting robust demand across our portfolio of cloud products supporting AI data centers,” says president & CEO Michael Hurlston. “The outperformance was broad-based across our cloud-focused business, with particular strength in components, specifically EML [electro-absorption modulated laser] chips, pump lasers, and narrow-linewidth laser assemblies for data-center interconnect [DCI], as well as 800G modules.”

Cloud & Networking segment revenue was hence $424.1m (88.2% of revenue), up 16.1% on $365.2m last quarter and 66.5% on $254.7m a year ago, led by exceptional hyperscale cloud strength. Specifically, cloud module revenue surpassed the 50% quarter-on-quarter growth target (accounting for about half of total revenue growth), with shipments to all three announced hyperscale customers. Record EML revenue nearly doubled from the fiscal Q4/2024 baseline, ahead of plan. Revenue from narrow-linewidth lasers (critical components for ZR and ZR+ modules) for DCI applications grew for a sixth consecutive quarter (with demand outpacing supply and expected to do so through the rest of fiscal 2026). Lumentum also saw sequential growth in shipments of other coherent components for long-haul data transmission, as well as in pump lasers for subsea terrestrial transmission, supported by robust cloud investment. It also continued shipments of ultrahigh-power lasers for co-packaged optics (CPO) solutions (prior to a broader ramp expected in calendar second-half 2026). The firm also achieved the first revenue from optical circuit switches (OCS) — with shipments to two customers, with a third committed for deployment in calendar-year 2026 — and accelerated in-house production for ramp-up in 2026.

Industrial Tech segment revenue was $56.6m (11.8% of revenue), down 5.7% on $60m last quarter but up 5.6% on $53.6m a year ago, with 3D sensing applications following seasonal patterns. Ultrafast laser demand was steady and at near record levels, driven primarily by strong demand from a leading tool supplier supporting high-volume solar cell manufacturing. Lumentum has also launched PicoBlade Core ultrafast laser platform, which enables infrared, green and ultraviolet wavelengths within a compact form factor for industrial micro-machining applications.

On a non-GAAP basis, quarterly gross margin has risen further, from 27.8% a year ago and 35.2% last quarter to 37.8%, raising full-year gross margin from 30.2% in fiscal 2024 to 34.7% for fiscal 2025. This was driven by improvements in product mix (as a result of increased datacom laser shipments) and by manufacturing utilization.

Reflecting annual employee cash incentives tied to company performance, along with ongoing investments to scale operations in support of expanding cloud opportunities, quarterly operating expenses have risen further, from $101.4m a year ago and $103.4m last quarter to $109.3m (comprising SG&A expense of $41.7m and R&D expense of $67.6m). However, as a proportion of revenue, this has been cut from 32.9% a year ago and 24.3% last quarter to 22.7%.

Cloud and networking segment profit margin has risen further, from 10.1% a year ago and 20% last quarter to 23.6%, due to higher revenue and favorable product mix.

Due to stringent cost initiatives, Industrial Tech segment profit margin has continued to rise, from 4.3% last quarter to 6% (despite lower revenue), up from just 0.4% a year ago.

Operating income has hence risen from $46.1m (operating margin of 10.8%) last quarter to $72.3m (15% operating margin), compared with an operating loss of $15.8m (-5.1% operating margin) a year ago. Full-year operating income was hence $160.1m (operating margin of 9.7%) for fiscal 2025, an improvement from an operating loss of $7.6m (–0.6% operating margin) in fiscal 2024.

Quarterly net income has risen from $40.9m ($0.57 per diluted share) last quarter to $63.3m ($0.88 per diluted share) for fiscal Q4/2025 (above the raised guidance), compared with $8.9m ($0.13 per diluted share) a year ago. Full-year net income has hence risen from $29.8 ($0.44 per diluted share) in fiscal 2024 to $146.4m ($2.06 per diluted share) for fiscal 2025.

In fiscal Q4, capital expenditure (CapEx) was $59m (up on $24m a year ago) focused on manufacturing capacity for cloud customers. Cash flow from operations for fiscal full-year 2024 was $24.7m.

During the quarter, total cash, cash equivalents and short-term investments rose by $10.4m, from $866.7m to $877.1m.

Inventory levels increased sequentially to support the expected growth in cloud and networking revenue.

September-quarter outlook

For fiscal first-quarter 2026 (to end-September 2025), Lumentum expects revenue to grow to a record $510–540m, driven by sequential growth in the Cloud & Networking segment (with strong growth across the portfolio of products addressing cloud and AI applications), as Industrial Tech segment revenue will be roughly flat (with a modest decline in industrial lasers offset by a seasonal uptick in 3D sensing). Operating margin should rise to 16–17.5%. Diluted earnings per share should increase to $0.95–1.10.

“We just received the largest single purchase commitment in company history for our ultra-high power lasers, and we have already announced additional investment in our US-based indium phosphide wafer fab to support it. Our investments in this facility will position us for a significant revenue ramp in CPO by 2026,” says Hurlston.

“Our wafer fab expansion is progressing on schedule, enabling us to support higher volumes of EMLs and other indium phosphide-based devices, including CW lasers and coherent components,” says Hurlston. “Recently, we received a substantial order for 200Gb/s-lane-speed EML chips, which we expect to fill in December. Overall, we expect 2026 to be a breakout year for laser chip sales of both 100Gb/s and 200Gb/s lane speeds,” he adds.

“While our manufacturing capacity for narrow-linewidth laser assemblies continues to ramp, demand is outpacing supply and is expected to do so through the rest of fiscal 2026,” says Hurlston.

Supply constraints persist in EML capacity and narrow-linewidth lasers, with management actively expanding fab capability and noting that pricing power should become a more meaningful factor as capacity ramps.

“We are positioning ourselves for longer-term growth, particularly in three significant areas: cloud modules, optical circuit switching, and co-packaged optics,” says Hurlston.

“We expect continued strong demand for our AI data-center and long-haul solutions, giving us confidence in surpassing $600m in quarterly revenue by June 2026 or earlier [with gross margin of at least 40% and operating margin above 20%, as per the long-term financial model outlined in April, through a combination of high-value products and disciplined cost management],” concludes Hurlston.

Lumentum expanding ultra-high-power laser production in San Jose

Lumentum quarterly revenue grows 10% year-on-year despite manufacturing capacity constraints