News: Optoelectronics

18 December 2023

Lumentum’s quarterly revenue falls due to inventory correction at networking customers

For its fiscal first-quarter 2024 (to end-September 2023), Lumentum Holdings Inc of San Jose, CA, USA has reported revenue of $317.6m, down 14.3% on $370.8m last quarter and 37.3% on $506.8m a year ago, but above the midpoint of the $300–325m guidance range.

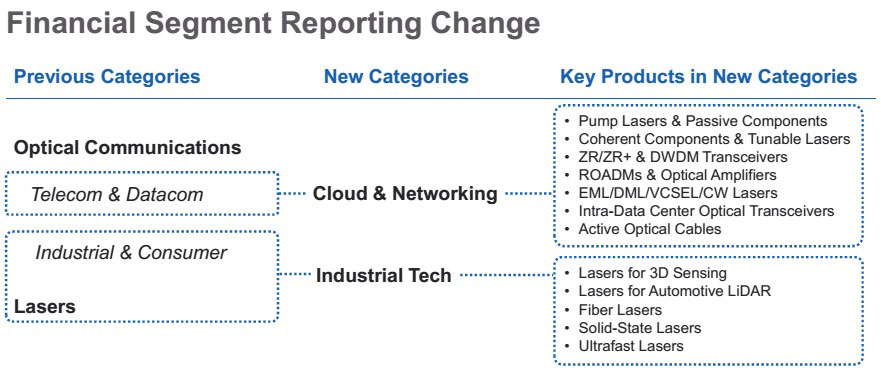

During the quarter, to better align with trends in its markets and its customer and product mix, Lumentum changed its organizational structure, from the two reportable segments ‘Optical Communications’ (OpComms) and ‘Commercial Lasers’ to ‘Cloud & Networking’ (Telecom and Datacom product lines from OpComms) and ‘Industrial Tech’ (the former Commercial Lasers segment plus the Industrial & Consumer product lines from OpComms).

Cloud & Networking segment revenue was $229.7m (72.3% of total revenue), down 19.8% on $286.5m last quarter and 36.2% on $360.1m a year ago. This was as expected, given the inventory correction underway at networking customers, with broad-based softness across most networking product lines, partially offset by sequential growth in intra-data-center lasers and tunable access module.

Industrial Tech segment revenue was $87.9m (27.7% of total revenue), down 40.1% on $146.7m a year ago (due mainly to more intense competition for market share on a certain 3D sensing socket, end-market demand and pricing) but up 4.3% on $84.3m last quarter (driven by the expected uptick in 3D sensing business with a new smartphone product ramp, partially offset by softness in fiber lasers as the firm’s leading fiber-laser customer works to bring down inventory).

“While we continue to see very strong growth in the demand for our data-center chips as well as our newly acquired intra-data-center transceivers, this strength is being offset by the telecom and industrial inventory drawdown activities,” says president & CEO Alan Lowe. “Due to this inventory correction, we believe we continue to ship below end-market demand.”

During fiscal Q1, there were again three greater-than-10% customers (two in the Networking segment and one in the Industrial Tech segment).

“As we navigate this transition period, we are delivering as planned on our product roadmaps and synergy attainment with respect to our NeoPhotonics acquisition [acquired in August 2022],” says Lowe.

On a non-GAAP basis, gross margin has fallen further, from 48.2% a year ago and 36.7% last quarter to 34.9%, due mainly to the lower revenue, factory under-utilization and product mix.

Operating expenses have been cut further, from $106.7m a year ago and $102.4m last quarter to $100.1m (31.5% of revenue), due to tight expense controls. SG&A expense was $39.1m. R&D expense was $61m.

Operating income has fallen further, from $137.4m a year ago (operating margin of 27.1%) and $33.7m (9.1% margin) last quarter to $10.6m (3.3% margin).

Likewise, net income has fallen further, from $119.2m ($1.69 per diluted share) a year ago and $40.2m ($0.59 per diluted share) last quarter to $23.4m ($0.35 per diluted share, but at the top of the $0.20–0.35 guidance range).

“First-quarter revenue and EPS results were above the midpoints of our guidance, and we are maintaining tight cost controls,” says Lowe.

However, during the quarter, cash, cash equivalents and short-term investments fell by $69.3m from $2013.6m to $1944.3m. The firm used $30m in cash to purchase its wafer fab and campus in the UK. “This purchase reflects our confidence in the longevity of indium phosphide technology to address the ever-growing need for higher and higher-performance telecom transmission components,” says chief financial officer Wajid Ali. To capture COGS synergies from the NeoPhotonics acquisition, Lumentum is pre-building nearly $30m of inventory to help facilitate the factory consolidation happening over the next few months. Also, the firm had an annual Japan tax payment of about $17m, as well as expenses related to the Cloud Light acquisition.

On 7 November, Lumentum completed its acquisition (announced at the end of October) of Cloud Light Technology Ltd of Hong Kong (which designs and makes optical transceiver modules for automotive sensors and data-center interconnect applications).

Hence, including the projected financial results of Cloud Light after the acquisition date, for fiscal second-quarter 2024 (to end-December 2023) Lumentum expects revenue to rise to $350–380m, with Industrial Tech down sequentially but Cloud & Networking up sequentially.

Operating margin is expected to be 2–4%, while diluted earnings per share should be $0.25–0.35.

To streamline operations and achieve synergies, Lumentum will be consolidating NeoPhotonics back-end manufacturing facilities, and hence expects under-absorption of capacity relating to these moves during fiscal Q2 and Q3/2024. “By the end of Q4, as we ramp up production of NeoPhotonics’ products within Lumentum’s manufacturing footprint, we expect to shift buffer inventory, enabling these manufacturing costs to align with the rest of our production,” says Ali. “In addition, as we continue to focus on cash generation, we expect our internal inventories to decline throughout the balance of the fiscal year.”

“The addition of Cloud Light’s products to our portfolio positions Lumentum as a leader in providing photonics to cloud operators at a time when artificial intelligence is rapidly accelerating growth in the data-center market. Lumentum’s served opportunity within data centers has expanded more than five-fold as a result of the Cloud Light acquisition,” says Lowe.

“For years, Cloud Light has been supplying differentiated high-speed products to leading hyperscale customers, both custom products to address unique customer needs, as well as standard products to address a broad range of hyperscale customer requirements. In the last 12 months, over 90% of Cloud Light’s revenue was derived from 400G-and-higher-speed products. In the most recent quarter, over half of Cloud Light’s optical transceiver revenue was derived from 800G transceivers,” he adds.

“In calendar 2024, we expect cloud applications will drive over 30% of our Cloud & Networking revenue, both within data centers and for data-center interconnect. We anticipate year-over-year Cloud & Networking growth in calendar 2024, driven by accelerating AI compute requirements, and as customer inventory levels are reduced and our shipment rate is more in sync with end-market demand.”

Lumentum completes acquisition of Cloud Light for $750m

Lumentum’s quarterly revenue falls 3.3% as customer inventory digested

Lumentum’s quarterly revenue falls 24.2% sequentially due to customer inventory digestion