News: Markets

6 December 2022

Automotive semiconductor chip market growing at 11.1% CAGR to over $80bn in 2027, driven by electrification and ADAS

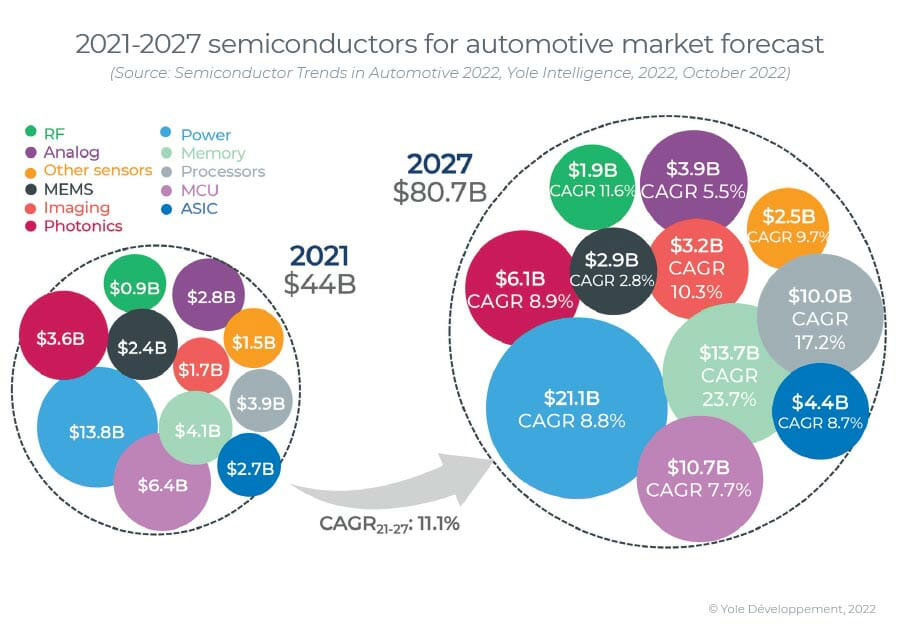

Despite a relatively flat market for light vehicles, the market for automotive semiconductor chips is rising at a compound annual growth rate (CAGR) of 11.1% from US$44bn in 2021 to US$80.7bn in 2027, reckons Yole Intelligence in its ‘Semiconductor Trends in Automotive 2022’ report. This represents the semiconductor chip value per car rising from ~US$550 to ~US$912 in 2027, while the number of chips incorporated in each car grows from ~820 to ~1100.

“The rapid increase in car electrification demands new types of substrates, such as silicon carbide (SiC) for power electronics. It is expected to represent 1130kwafers in 2027,” says Pierrick Boulay, senior technology & market analyst in the Photonics and Sensing Division at Yole Intelligence. “While still low compared to the ~30,500kwafers of silicon expected for 2027, silicon carbide will grow faster than silicon and gallium arsenide (GaAs)/sapphire,” he adds. “ADAS is also an important driver, and micro-controller unit (MCUs) with cutting-edge technology as low as 16nm/10nm will go into ADAS (advanced driver assistance systems), including radar and other sensor controls. Levels 4 and 5 of autonomy will drive increasing demand for more memory (DRAM) and computing power.”

For electrification, vertical integration is becoming popular among OEMs. It can work out in multiple ways: full integration down to the component level, system integration and subcontracting build-to-print parts, strategic cooperation/direct investments with key component suppliers, etc. The conventional automotive supply chain needs to examine its position thoroughly and transform through joint ventures, mergers & acquisitions (M&As), and new investments and divestments to retain its competitive edge, reckons Yole Intelligence. Although semiconductors are critical to the automotive industry in the ongoing disruptive transition, most players, both OEMs and tier-1 suppliers, do not yet have well-defined strategies for semiconductors. Specific expertise in semiconductor technologies and their supply chains, both internally and externally, is urgently needed to prepare for the future.

“Supply chain management will change as OEMs will need to negotiate directly with chip manufacturers, learn from the consumer industry, and keep ‘buffer stock’,” says Eric Mounier Ph.D., director of market research at Yole Intelligence. “They must work closer with chip manufacturers on volume forecasts and long-term orders,” he adds. “Just-in-time manufacturing, pioneered by Toyota in the 1960s, no longer works with chip manufacturers in the current geopolitical climate.”