- News

30 October 2019

Aixtron year-to-date revenue grows despite export license delays hitting Q3

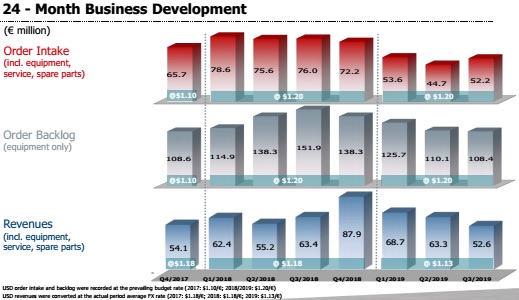

For third-quarter 2019, deposition equipment maker Aixtron SE of Herzogenrath, near Aachen, Germany has reported revenue of €52.6m, down 17% on €63.3m last quarter and €63.4m a year ago, due partly to longer-than-expected processes involved with obtaining export licenses for some of customers.

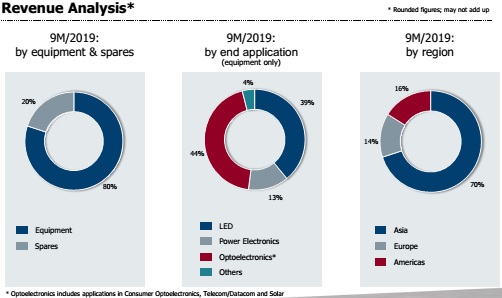

Nevertheless, sales for the first nine months were up 2% year-on-year, from €180.9m to €184.6m. Of this, equipment rose from €145.4m to €148.1m (remaining 80% of total revenue), while spare parts & services rose from €35.5m to €36.5m.

On a regional basis, revenue from Asia rose year-on-year by 42% from €90.9m to €128.8m (rebounding from just 50% to 70% of total revenue), while Europe fell by 53% from €54.2m to €25.6m (going from 30% to 14% of total revenue) and the Americas fell by 16% from €35.8m to €30.2m (going from 20% to 16% of total revenue).

Of equipment revenue, metal-organic chemical vapor deposition (MOCVD) systems for ‘Optoelectronics’ (consumer optoelectronics, telecom/datacom and solar) contributed 44%, systems for ‘LEDs’ 39%, and systems systems for ‘Power Electronics’ 13%.

Gross margin for the first nine months fell year-on-year from 43% to 40% due to a change in the product mix. However, despite still being down from 44% a year ago, quarterly gross margin recovered slightly from 41% in Q2 to 42% in Q3/2019. This was despite the effect of the low level of sales in relation to fixed costs, because of the continuing strong dollar, a good sales mix with a lower proportion of shipments into the display market, and continuing cost improvements.

Operating expenses for the first nine months have been cut by 13% year-on-year, from €57.6m to €50.2m (including €16.7m in Q3), due mainly to other operating income rising to €5m (driven largely by higher R&D grants received of €2.2m, counteracting R&D spending rising from €12.5m in Q2 to €14.7m in Q3). “The further reduction in costs as well as the still advantageous USD/€ exchange rate are helping us to achieve our targets,” says president Dr Bernd Schulte.

Despite operating result (EBIT) falling from €9.3m (15% of revenue) in Q2 to €5.5m (10% of revenue) in Q3, EBIT for the first nine months improved year-on-year by 18% from €20.7m (11% of revenue) to €24.5m (13% of revenue), due mainly to the business and cost developments.

Quarterly net profit has fallen further, from €11.7m a year ago and €7.3m (12% of revenue) in Q2 to €4.4m (8% of revenue) in Q3. Net profit for the first nine months fell year-on-year from €27.7m (15% of revenue) to €20.2m (11% of revenue), although the prior-year period was positively impacted by the recognition of deferred tax assets of €9m.

Despite operating cash flow falling further, from €13.9m a year ago and €13.6m in Q2 to €4.9m in Q2, operating cash flow for the first nine months rose year-on-year from €5.4m to €6.5m.

Capital expenditure (CapEx) has risen from €1m in Q2 to €2.6m in Q3, taking CapEx in the first nine months of 2019 to €9.2m (up year-on-year from €6.8m).

Free cash flow in the first nine months hence worsened year on year from -€1.4m to -€2.7m, due mainly to the increased working capital (including investment in beta tools) as well as the growth of inventories, and reflecting the current order situation. Quarterly free cash flow also fell from €12.6m in Q2 to €2.3m in Q3.

Cash and deposits (with a maturity of at least three months) hence rose during Q3 from €258.9m to €260.6m, although this is still slightly below the €263.7m at the end of 2018.

Order intake (including spare parts and service) in the first nine months fell 35% year-on-year, from €230.3m to €150.6m as a result of the reluctance of customers to invest in capacity expansion. However, orders recovered in Q3 to €52.2m, up 17% on the trough of €44.7m in Q2, due mainly to demand for datacom lasers as well as silicon carbide (SiC) and gallium nitride (GaN) power electronics.

So, despite being down 29% on €151.9m a year previously, equipment order backlog of €108.4m (as of 30 September) was down just 2% on €110.1m at the end of Q2.

“The increased order intake in the third quarter makes us optimistic that we will achieve our targets for the current fiscal year,” says Schulte. Despite low visibility, increases in both revenue and order intake are expected in Q4/2019. Based on customer agreed shipment schedules and despite the issues with the export license, Aixtron expects Q4 revenue to increase to the highest level for 2019. “In Q4, assuming no further export delays, we expect to meet our guidance of a positive free cash flow of around €15m,” notes VP of finance & administration Charles Russell.

The market developments of an increasing use of lasers for optical data transmission and 3D sensor technology, a progressive expansion of the 5G network and an increasing use of energy-efficient power electronics remain positive and are reflected in ongoing customer discussions, says Aixtron.

“We continue to assess the medium- and long-term prospects for our core markets in optoelectronics and power electronics as positive,” comments president Dr Felix Grawert. “As the market and technology leader in optoelectronics, we are in an excellent position both in laser and special LED applications as well as in power electronics,” he believes.

As part of the review of its technology and product portfolio, at the end of September Aixtron officially unveiled its new fully automated AIX G5 WW C silicon carbide epiwafer production system. “We have received positive customer feedback and initial orders in recent months,” notes Grawert.

In addition, Aixtron’s organic light-emitting diode (OLED) subsidiary APEVA is working with customers to prove the performance of the organic vapor phase deposition (OVPD) technology. “Our Gen2 OLED system is being operated in a pilot production line at our customer’s plant jointly by engineers from our customer and our subsidiary APEVA in a pilot-production line,” says Grawert. “Intensive efforts are being made to optimize the system as well as the process parameters for manufacturing OLEDs using the OVPD process. This is expected to confirm the performance of the OVPD technology in the coming months and create the data required for the customer’s decision to place a follow-up order for a further OVPD tool - even if we do not expect this in the current fiscal year.”

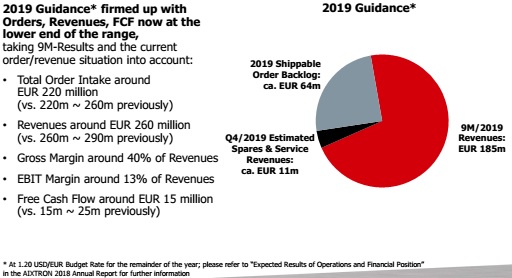

Based on the revenue of €185m in the first nine months of 2019, assessment of the development of demand in the current market environment (including estimated Q4 spares & service revenue of about €11m and 2019-shippable order backlog of about €64m) and the budget exchange rate of 1.20 $/€, for full-year 2019 Aixtron now targets the bottom of its previous guidance ranges for revenue (€260-290m), orders (€220-260m) and free cash flow (€15-25m). “Due to the uncertain timing of granting the export license as well as the potential OLED order and respective revenues having been shifted into next year, we have set our expectation on orders and revenues and, as a consequence of that also on the free cash flow, to the low end of the respective original ranges,” explains Schulte.

However, due to cost control and the strength of the US dollar, Aixtron still expects gross margin of about 40% and EBIT of about 13% of revenue (margin of around 13%, both at the top end of the originally guided ranges).

This forecast accounts for the longer-than-expected review processes for granting export licences as well as the follow-up OLED order no longer being expected in 2019. Expectations fully include the results of Aixtron’s APEVA subsidiary, including all necessary investments to continue the development of OLED activities.

“Developments in Aixtron’s markets are positive,” concludes the firm. “In particular, the increasing use of lasers in optical data transmission and 3D sensor technology, the expansion of the 5G network and the increasing use of energy-efficient power electronics are expected to lead to further growth in the corresponding target markets.”

Aixtron presents next-gen AIX G5 WW C SiC epi production system

Aixtron’s Q1 gross margin and earnings exceed expectations

Aixtron full-year revenue up 40% organically to €268.8m

Aixtron’s revenue grows 15% in Q3, driven by power electronics, laser and ROY LED applications