- News

10 May 2019

Veeco’s Q1 revenue levels out at $99m after drop off of commodity LED MOCVD system sales to China

For first-quarter 2019, Epitaxial deposition and process equipment maker Veeco Instruments Inc of Plainview, NY, USA has reported revenue of $99.4m, down 37% on $158.6m a year ago but roughly level with $99m last quarter (and above the midpoint of the $85-105m guidance range, driven by strength in services business). “With the commodity LED business [which includes the sale of metal-organic chemical vapor deposition (MOCVD) systems to the China LED market] largely behind us, our revenues for the quarter have stabilized,” notes CEO Bill Miller.

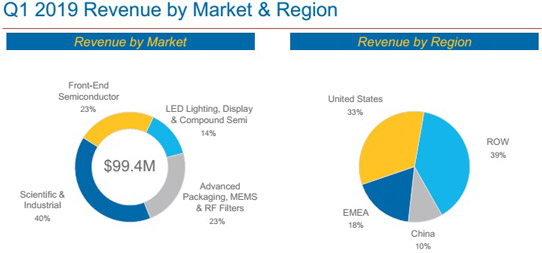

With almost no contribution from commodity LED equipment sales (as expected), the LED Lighting, Display & Compound Semiconductor segment remained just 14% of total revenue (following the plunge from 46% in Q3/2018 to 14% in Q4/2018). Most of the segment’s revenue was therefore in Compound Semiconductors, including MOCVD systems for specialty LEDs, automotive, photonics and power electronics applications.

The Advanced Packaging, MEMS & RF Filter segment – including lithography and Precision Surface Processing (PSP) systems sold to integrated device manufacturers (IDMs) and outsourced assembly & test firms (OSATs) for Advanced Packaging in automotive, memory and other areas – has rebounded from a low of just 14% of total revenue last quarter to 23%, driven by multiple Advanced Packaging lithography systems sold for high-bandwidth memory as well as CPUs and other applications.

The Front-End Semiconductor segment (formerly part of the Scientific & Industrial segment, before the May 2017 acquisition of lithography, laser-processing and inspection system maker Ultratech Inc) has risen slightly from 22% of total revenue last quarter to 23%, driven by multiple laser spike anneal (LSA) systems shipped to a leading foundry for process steps at an advanced technology node.

The Scientific & Industrial segment has fallen back from last quarter’s high of 50% of total revenue to 40%, driven by shipments to data storage customers as well as several ion beam sputtering systems shipped to optical customers.

Geographically, the quarter saw slight rebounds in China from just 9% to 10% of total revenue and in Europe, Middle East & Africa (EMEA) from just 17% to 18%. Meanwhile, the USA has fallen back from 41% to 33%, while the rest of the world (which includes Japan, Taiwan and South Korea) has risen further from 33% to 39%.

On a non-GAAP basis, gross margin has fallen further, from 36.5% a year ago and 36% last quarter to 35.5% (albeit towards the high end of the 34–36% guidance range, driven by tighter spending controls). Operating expenses were cut further, from $46.5m a year ago and $42.6m last quarter to $40m (better than the targeted $41m). “Our cost-reduction efforts were achieved a quarter earlier than previously communicated,” notes chief operating officer & chief financial officer Sam Maheshwari.

Despite still being well below net income of $9.2m ($0.20 per diluted share) a year ago, net loss has been cut from $7.5m ($0.16 per diluted share) last quarter to $6.4m ($0.14 per diluted share), above the midpoint of the expected range of $14–5m ($0.30–0.10 per share).

“We are executing according to our plan, with Q1 revenue and EPS results above the midpoint of our guided range,” says Miller.

Due mainly to the $6.4m net loss as well as working capital investments and biannual debt interest payment, cash flow from operations has worsened from $2m last quarter to cash outflow of –$22m. Capital expenditure (CapEx) was $2.2m. During the quarter, cash and short-term investments have hence fallen by about $24m, from $261m to $237m (of which $66m is held offshore).

Order bookings were $107.2m. “We saw strength in Scientific & Industrial orders, driven by our data storage customers,” notes Maheshwari. “We also received multiple advanced packaging lithography system orders and another EUV [extreme ultraviolet] mask-blank [ion beam deposition] system order [the firm’s fifth production-capacity order – the first was shipped in April].” Despite bookings being down 4.3% on $112m last quarter, order backlog grew from $288m to $295m.

For second-quarter 2019, Veeco expects revenue to be steady, at $90–110m. Gross margin should recover to 37–39%. With OpEx remaining about $40m, net earnings are expected to range between a loss of $9m ($0.18 per diluted share) and a profit of $1m ($0.02 per diluted share). Although the cash balance declined during Q1, Veeco expects to generate positive cash flow in Q2/2019.

“Based on our backlog and current visibility, we see Q3 sales tracking above Q2,” says Maheshwari. “We also see our gross margins further improving due to favorable product mix,” he adds. “For the second half of 2019, we see top-line improving over the first half by roughly 10%. We continue to target gross margin of 40% by the end of this year.”

Veeco’s growth initiatives (which align with multiple megatrends) comprise: ion beam deposition systems for EUV mask blanks and laser annealing for advanced wafer processing (Front-End Semiconductor); MOCVD (Compound Semiconductor) for 3D sensing/VCSELs (vertical-cavity surface-emitting lasers); and lithography for wafer-level packaging (Advanced Packaging).

“On our MOCVD technology applied to the VCSEL market, we have been enhancing our TurboDisc platform to produce high-performance epitaxial VCSEL stacks,” says Miller. “We are currently working with multiple customers to place the beta tool in their facilities [expected in the near term],” he adds. “This market today is absorbing the capacity that was recently added for the smartphone facial recognition application. However, we believe that additional 3D sensing applications such as world-facing sensors and automotive LiDAR will generate demand for some time. This is a potential market opportunity of $100–150m per year.”

“Looking ahead, we remain confident about growing our top line and returning to profitability,” concludes Miller.

Veeco’s revenue falls 22% in Q4/2018 due to commoditization of China LED MOCVD market

Veeco’s Q3 revenue down more than expected due to China market softness

Veeco’s revenue grows 14% in Q1 to $158.6m, driven by MOCVD system shipments to China