- News

19 June 2018

Finisar’s quarterly revenue falls 6.7% due to lower demand from Chinese OEMs

© Semiconductor Today Magazine / Juno PublishiPicture: Disco’s DAL7440 KABRA laser saw.

For full-year fiscal 2018 (ended 29 April), fiber-optic communications component and subsystem maker Finisar Corp of Sunnyvale, CA, USA has reported revenue of $1316.5m, down 9.2% on fiscal 2017’s $1449.3m, due mainly to lower demand from Chinese OEM customers. In particular, Datacom product sales fell by 1.2% to $12.8m, while Telecom product sales were fell by 29.5% to $120m.

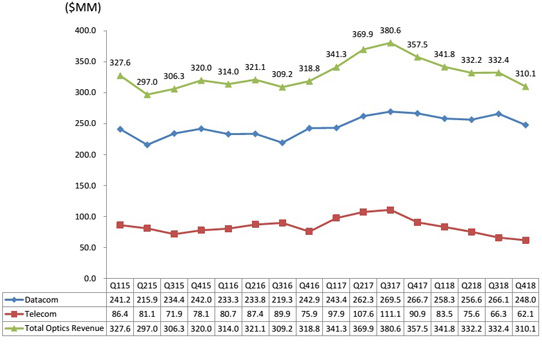

Fiscal fourth-quarter revenue was $310.1m, down 6.7% on $332.4m last quarter and 13.3% on $357.5m a year ago. Datacom product sales were $248m, down 6.8% on $266.1m last quarter, due mainly to the expected decline in revenue from vertical-cavity surface-emitting laser (VCSEL) laser arrays for 3D sensing applications. Telecom product sales were $62.1m, down by 6.4% on $66.3m last quarter (due mainly to the full three-month impact of the annual telecom price reductions) but also down 31.7% on $90.9m a year ago.

Like last quarter, Finisar had two 10%-or-greater customers. The top 10 customers represented 61.1% of total revenue (down from 63.3% last quarter).

Graphic: Finisar’s quarterly revenue trends.

On a non-GAAP basis, gross margin has fallen further, from 36.2% a year ago and 28.6% last quarter to 24.7% (well below the expected 27-28%). This is due to the impact of the full three months of the telecom price reductions, under-absorption of fixed manufacturing expenses in the VCSEL laser fab in Allen, Texas, and an increase in non-cash inventory reserves. Full-year gross margin hence fell from 35.9% to 29.7%.

Full-year operating expenses rose from $280.3m (19.3% of revenue) to $292.2m (22.2% of revenue). Although up from $71m a year ago, fiscal Q4 operating expenses were $72m, cut slightly from $72.4m last quarter.

Despite this, operating income fell further, from $58.4m (operating margin of 16.3% of revenue) a year ago and $22.7m (6.8% margin) last quarter to $4.6m (1.5% margin, well below the expected 4%). Full-year operating income was hence down from $240.6m (16.6% margin) to $99.2m (7.5% margin).

Likewise, net income has fallen further, from $57.5m ($0.50 per diluted share) a year ago and $22.8m ($0.20 per diluted share) last quarter to $5.8m ($0.05 per diluted share, below the expected $0.09-0.15). Full-year net income hence fell from $231.7m ($2.03 per diluted share) to $100.4m ($0.86 per diluted share).

Capital expenditure (CapEx) was $55.2m (above the forecasted $45m). This included $4.4m for ongoing construction of the third building of Finisar’s manufacturing site in Wuxi, China (due for completion in calendar second-half 2018) and $27m on uplift of the new 700,000ft2 facility in Sherman, Texas (purchased recently in order to expand manufacturing capacity for VCSELs using 6-inch wafers) and the initial deliveries of capital equipment for that site.

During the quarter, cash and short-term investments hence fell from $1.216bn to $1.197bn.

“While we are disappointed in last quarter’s results, we do expect both revenues and gross margins will increase in our fiscal first quarter,” says CEO Michael Hurlston.

For fiscal first-quarter 2019, Finisar expects revenue to grow slightly to $305-325m. There should be improvements in gross margin to 26-27%, operating margin to 4-5%, and earnings per fully diluted share to $0.10-0.16.

Excluding $100m for the uplift of the building and additional equipment at the Sherman facility, CapEx should be $30m. This includes $5m related to the construction and fit out of the third building in Wuxi.

“We expect to see an increase in demand for our VCSEL laser arrays for 3D sensing applications in the second fiscal quarter in connection with the expected timing of the new product introductions by our customers,” notes Hurlston. “In addition, we have closed a number of design wins for our VCSELs in consumer and automotive applications,” he adds. “Our opportunity funnel will continue to increase in areas beyond automotive and handsets. We continue to make progress with respect to uplift of the building and the ordering and receipt of capital equipment for VCSEL laser fab in Sherman, Texas for 3D sensing applications and still expect to be qualified and in production using 6-inch wafers by the end of the calendar year, which we expect to significantly increase our production capacity.”

“In our core business, we’re seeing increased demand for ROADMs [reconfigurable optical add/drop multiplexers] as India and China deploy more advanced networks. In our datacom transceiver business, we’re seeing increased unit volumes in the data-center market, but this is being offset by continued ASP [average selling price] pressure. We have a set of cost reductions and process to provide greater pricing flexibility,” Hurlston says.

“We have begun to make changes at Finisar that I believe will not only bring more focus to our product development efforts, but will lead to better execution and efficiency, allowing the company to reduce relative expense levels,” says Hurlston. “We can ultimately get to a sustainable operating margin of 12-15%. We plan to do this by ramping in new markets, changing our product mix and focusing R&D priorities,” he adds. “Fundamental to achieving this objective will be managing our operating expenses to 18-20% of revenue… We’ll take multiple quarters to implement, but we have already begun taking steps to execute a plan consistent with these objectives.”

“On the horizon, we believe we are well positioned with the major 5G wireless OEMs on 25G and 100G data rates for both short- and long-reach applications,” reckons Hurlston. “We also believe we are well positioned for the 400G transition starting in calendar year 2019.”

Finisar’s sees lower quarterly telecom revenues from Chinese OEMs