- News

26 September 2017

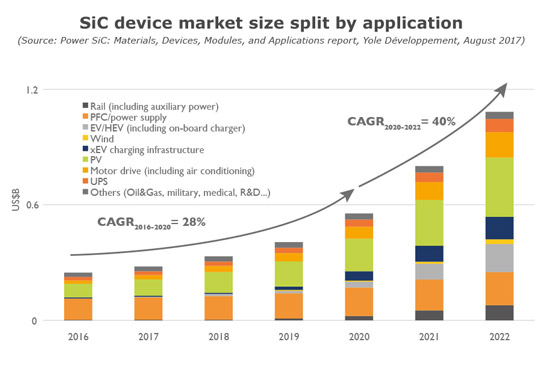

SiC power device market to grow at 40% CAGR from 2020 to more than $1bn in 2022, after tipping point in 2019

“The SiC power business is concrete and real, with a promising outlook,” said Yole Développement in 2016. The trend has not changed in 2017, and the SiC industry is going even further as industrial players have increasing confidence about the SiC power market, adds the market analyst firm in the third edition of its SiC technology & market analysis: ‘Power SiC 2017: Materials, Devices, Modules, And Applications’. End users were once simply curious about SiC, but they are now coming to try it, building prototypes for concrete projects that could drive volumes in coming years.

“SiC technology’s added value is today widely understood and accepted by the power electronics community,” comments technology & market analyst Dr Hong Lin. “We are gradually going from the customer awareness and education stage to the customer trial and adoption stage. And this is especially true for SiC transistors.”

Besides the general positive feedback, multiple other signals reveal that the market adoption of SiC power devices is going to accelerate.

The power factor correction (PFC)/power supply segment is still the leading SiC application. However, its market share is expected to decrease gradually because of the penetration of new applications of SiC.

Photovoltaic (PV) applications seem are broadly adopting SiC products. Indeed, SiC solutions offer a better performance/cost ratio at the system level for string PV inverters. Yole has identified players that are already using SiC MOSFETs and diodes.

In the future, electric vehicle (xEV)-related applications, rail and others are also expected to contribute to the market evolution.

The leading Chinese xEV manufacturer BYD has confirmed that it is using SiC in its on-board chargers. SiC is now on the road, not only on trial. While the on-board charger is embracing SiC technology, the pre-2020 market volume for SiC devices in automotive applications will mainly be limited to on-board chargers.

On the other hand, for the main inverters the situation remains the same as 2016: almost all the OEMs and tier-1 firms are testing SiC devices. Some pioneers like Toyota, Nissan and Honda will probably launch SiC-based solutions around 2020. After 2020, due to the high power rating of the main inverter, even a low adoption rate will contribute to significant revenue after 2020, forecasts Yole.

Together with the development of the xEV market, the charging infrastructure market is emerging. Globaly, charging infrastructures are rapidly being deployed in the European Union (EU), USA and Japan, which will contribute to growth in SiC power device markets. Various players have confirmed adoption of their devices in xEV charging infrastructure. However, the development is especially impressive in China.

In this context, for a third time since 2014, Yole has increased its forecast for the SiC power device market, in particular for the post-2020 period after 2019 represents a tipping point in SiC adoption. While the market is growing at a 28% CAGR from 2016 to 2020, it will accelerate to 40% CAGR for 2020-2022, exceeding $1bn.

An established but evolving SiC power device supply chain

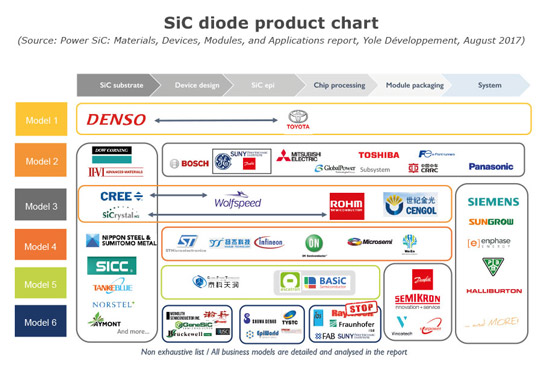

Looking back 16 years to the beginning of the commercialization of the first SiC power devices, only two companies offered them: Infineon and Cree (whose power and radio-frequency device business has since been spun out as Wolfspeed). The device market landscape did not really evolve for the next 10 years, as SiC struggled to prove itself to the industry.

The situation has taken a sharp turn since 2009-2010, with ever more device players supplying SiC diodes. As of July, the total number of diode suppliers is up to 23. The total number of SiC transistor suppliers is also increasing. In particular, it is worth highlighting that from 2016 to 2017 the number of SiC MOSFET suppliers has doubled. That number will undoubtedly further increase in the coming years, believes Yole.

As the device market has developed, an industrial supply chain has been established, from wafer to epitaxy, chip manufacturing, and module packaging and finally reaching system end users with different business models, for example:

- Wolfspeed and Rohm Semiconductor are vertically integrated from substrate to module;

- Mitsubishi Electric and Fuji Electric are vertically integrated from chip to end system;

- many other players occupy part of the supply chain.

This industrial supply chain is constantly evolving, with newcomers and quitters. In 2016-2017 in particular, Yole notes the following:

- At the wafer level, Dow Corning has been restructured after being acquired by Dow. The merger of Dow and Dupont now puts a question mark over the future of Dow Corning’s SiC wafer business (one of the main SiC suppliers). Also notable is the acquisition of Norstel by Chinese capital: the firm is now constructing a new factory in Fujian, China to expand its capacity.

- Despite the fact that Raytheon stopped its SiC foundry service in 2017, a foundry model is clearly in operation. This is helping fabless/fab-lite SiC companies to launch their products and make SiC technology more accessible to the industry. The model is currently driven by X-Fab, which is supported by Power America. Yole is expecting other foundries to enter the market too.

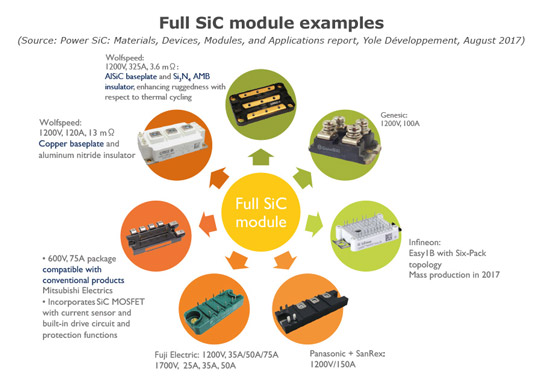

SiC modules are coming

As of 2017, the SiC power market is still dominated by discrete devices, including both discrete diodes and transistors. But that situation will change, reckons Yole. Hybrid modules are already penetrating some applications, such as PV, and full SiC modules are coming.

SiC transistors are especially advantageous for high-voltage, high-power-rating applications. Markets that are going to drive SiC include rail, motor drives, xEV and inverters, which all prefer modules. Yole therefore expects modules to gain market share. Indeed, SiC power semiconductor suppliers are taking action. Developments in the 2016-2017 period included the following:

- Number-one power semiconductor manufacturer Infineon has entered mass production of full SiC modules; and

- GE has teamed up with Danfoss for SiC module production.

Module players are not only launching products but also doing what they can to facilitate market adoption. For example, the launch of new modules is frequently associated with the release of driver electronics, assisting designers in surmounting the difficulties linked to the driver. Additional integrated ‘plug-and-play’ solutions (power stacks, power assemblies or power blocks) are appearing on the market. These help those end users who want to implement SiC modules in their products but do not have internal design resources or capabilities, notes Yole.

SiC power market growing at CAGR of 19% to 2021 as it spreads to more applications

www.i-micronews.com/compound-semi-report/product/