- News

7 October 2014

PFC, PV inverter and now rail applications fueling SiC market

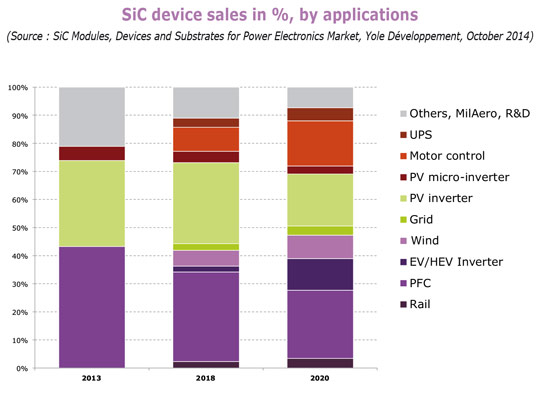

The market for silicon carbide (SiC) chips reached almost $100m in 2013 due to already well-established power factor corrector (PFC) applications, which still demands large volumes of diodes, according to Yole Développement. Secondly, photovoltaic systems, despite a depressed market, are the beachhead for new SiC-powered inverter or micro-inverter line-ups, says the market research firm in its new report ‘SiC Modules, Devices and Substrates for Power Electronics Market’. In addition, SiC is propagating over all industrial segments, it adds.

For example, rail applications such as train traction has surprisingly adopted SiC sooner than expected. This strategic choice has been made by industrials because of the availability of 1.7kV full and hybrid modules that have been demonstrated and installed by Mitsubishi Electric in Japan. Train applications could expand at a compound annual growth rate (CAGR) of more than 80% over 2015-2020. “Indeed, we expect other rolling-stock manufacturers will quickly adopt SiC, firstly in metro and then in the high-speed trains,” says Dr Philippe Roussel, business unit manager at Yole.” We also forecast PV inverters to keep on implementing SiC at an annual growth rate of almost 12%”, he adds.

The adoption of SiC in train applications is a major factor in the SiC industry. “It shows that SiC could play an important role in the high- and very high-voltage ranges, more than 1.7kV,” says Dr Hong Lin, technology & market analyst, Compound Semiconductors & Power Electronics, who remains convinced that these voltage and related power ranges “are exactly the place-to-be for SiC technology... Such technology can bring real added-value, despite a price positioning that differs from silicon,” he reckons. Here, savings are made at the system level, where passives and other cooling can be dramatically reduced when moving to SiC, Lin notes.

In its 2014 analysis of the SiC market, Yole also takes into account the competition with gallium nitride (GaN) devices in the PFC area. Now able to answer the needs of the 600V segment, GaN is becoming a serious competitor for SiC technology, the firm notes. Yole’s analysts therefore remain quite conservative regarding this application, which could switch to nitrides in the coming years.

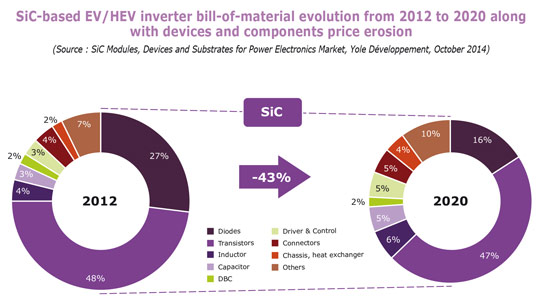

SiC in EV/HEV delayed beyond 2018

It has always been said that SiC could play a major role in EV/HEV power electronics. Most car makers agree that there is a 10% fuel saving when moving from silicon to SiC in hybrid vehicles. For a pure electric car this metric (for a given battery pack) will translate into lower battery consumption or extended range. It is now obvious that EV/HEV could easily capture the biggest portion of the SiC business, says Yole.

However, even though all technical indicators are green, the car industry is reluctant to implement SiC, claiming that the economics are not yet fully compatible with their expectations. “Such conservatism heavily impacts our previous predictions,” says Yole. According to key industrial voices (Toyota, Denso, Honda, Nissan etc), SiC will only be on the short list by 2018 for the most optimistic players and by 2020 for others. “By adding GaN 600V normally-off (Noff) devices (now in the starting blocks), we approach the most conservative scenario we developed in the past years, exhibiting a SiC device business in 2020 that will exceed $400m,” says Yole.

6-inch SiC wafers for power electronic applications to arise in 2016-2017

For n-type substrates, 4” wafers are the mainstream product on the market. The introduction of 6” n-type substrates in power electronic devices is slower than expected, says Yole. The quality of 6” wafers seems to still be an issue and the price is highly dependent on the quality, varying from $1300 to $2000. Additionally, the supply of 6” wafers is still limited.

The ratio between the price of 6” and 4” n-type substrates is about 2.5x, which is still too high and does not make 6” wafers appealing to device makers, despite their intention to transition to 6” in order to reduce device cost. The price of 6” n-type wafers is expected to drop quickly in the next two years and fall below the $1000 threshold. The large-scale transition to 6” is expected to take place in 2016-2017.

Concerning the players in SiC wafers, Cree remains the market leader by far. II-VI, Dow Corning and SiCrystal follow. Asian players are gaining market share little by little, but their volumes are still small compared to the leading players.

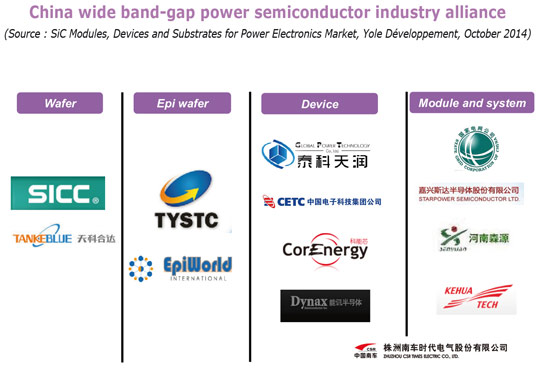

Chinese players entering the SiC field

China is already a big player in the power electronics field with most of the integrators. At the device level, the country has invested significant amounts in the R&D and production of insulated-gate bipolar transistors (IGBTs) in recent years. However, compared with the USA, Europe and Japan, China still has some way to go.

China is hoping to catch up with USA, Europe and Japan in the power electronics field, through the so-called ‘third generation of semiconductors’ (SiC and GaN etc). Consequently, the Chinese government has provided significant funding for SiC R&D and industrialization. Since 2006, several companies have gradually entered the SiC arena. Now, there are Chinese firms spanning the entire value chain, from materials to devices. In particular, in Asia, Japan leads SiC activities, but China is catching up and Korea is coming, notes Yole.

SiC power device market grows at 38% year-on-year, despite 2012’s overall power electronics downturn

Electric vehicle go-slow hits SiC power devices

www.i-micronews.com/compound-semi-report/