| Home | About Us | Contribute | Bookstore | Advertising | Subscribe for Free NOW! |

| News Archive | Features | Events | Recruitment | Directory |

News

6 July 2010

LED market to grow from $7bn in 2009 to $10.7bn in 2010 then $20.4bn in 2012

The LED market made a great leap in second-half 2009, expanding dramatically from US$7bn in 2009 to US$10.7bn in 2010 (a growth rate unattainable by any other electronic product), according to the ‘Global and China LED Industry Report 2009–2010’ from market research firm Research In China.

On the one hand, the penetration of LED backlighting into notebook PCs has surged from 15% at the end of 2008 to about 60%, and is expected to hit 88% (or 98% according to some predictions) by the end of 2010. On the other hand, the use of LED backlighting in LCD TVs has increased from 0.01% at the end of 2008 to 10% currently, and is expected to reach 27% at the end of 2010, while the use of LED backlighting in LCD displays has grown from just 0.01% at the end of 2008 to 5%.

Along with increasing LED brightness and falling prices, the penetration of LEDs into general lighting is expected to increase greatly; the general lighting market is of huge potential, with the market reaching US$100bn. Promisingly, the LED market is expected to reach $20.4bn in 2012.

Research In China categorizes the global LED market as falling into three camps. The first consists of Japan, Europe and the America, encompassing the world's five biggest LED makers — Nichia, Toyoda Gosei, Lumileds, Cree and Osram — as well as Toshiba, Panasonic and Sharp, and possessing high-end technologies and abundant patents, as well as being dedicated to the ultra-high-brightness UHB-LED field for many years (targeting both general lighting and automotive lighting markets). Japanese enterprises pay little attention to LEDs for the backlights of consumer electronics, says the report, while European and American enterprises show no interest at all.

The second camp consists of manufacturers in South Korea and Taiwan. With an integrated supply chain and interest in LEDs for backlighting consumer electronics, firms are experiencing rapid growth despite the gap to European and American enterprises in terms of technology.

The third camp consists of LED manufacturers in mainland China, which are small scale, scattered and low-tech. For example, there are no more than five packaging plants in South Korea, whereas in mainland China there are nearly 1000, many of which deal with resin packages of minimum technical content and few of which are engaged in SMD packaging.

The annual revenue of all these manufacturers fails to reach that of Taiwan's leading LED firm Everlight, and there are also large discrepancies between Everlight and South Korean manufacturers. Mainland China LED makers possess low-level technologies, with many producing quaternary green/yellow LEDs (mainly for outdoor landscape lighting, decoration or advertising). Mainland China is the world’s largest consumer electronics production base, but the purchasing right is centralized in the hands of Taiwanese and South Korean manufacturers. As a result, mainland manufacturers can see the rapid development of the LED market in consumer electronics but cannot benefit from it. As for general lighting, it is more beyond their reach due to their low-level technology, says the report.

Mainland China manufacturers cannot share in the highest-growth LED market, but they have the greatest enthusiasm for investment, with LED projects starting up everywhere, adds the report. Large numbers of metal-organic chemical vapor deposition (MOCVD) epitaxial growth systems for fabricating LEDs have been bought, with the LED project in Wuhu alone needing more than 200.

Shipments of MOCVD systems worldwide are forecasted to reach 662 units in 2010 (equivalent to the total for the previous three years). Promisingly, 2011 will maintain or even exceed this number. The unit selling price of an MOCVD system is $1–2m, and the Chinese government in particular offers a subsidy of up to 50%, so there is currently an upsurge of LED-related investments and a boom in MOCVD purchases in China. In 2010, the number of MOCVD systems registered with the National Development and Reform Commission (NDRC) alone is nearly 700, and some manufacturers purchase directly rather than wait for the NDRC subsidy. The MOCVD equipment market is dominated by Germany’s Aixtron and the USA’s Veeco Instruments, but the output capacity of both firms is limited, so order periods stretch into 2012.

However, Research In China warns that it is not easy for LED start-ups to produce qualified products, and there are many thresholds for LED patents. So, incaution can cause trouble, with some firms (in particular Nichia) often resorting to patent lawsuits.

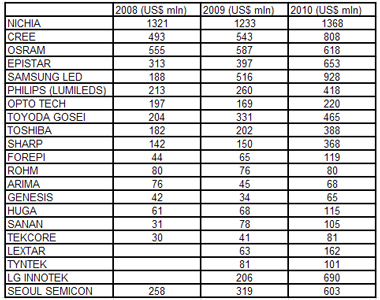

Chart: The world’s 21 biggest LED epitaxy manufacturers by revenue, 2008–2010.

See related items:

Taiwanese LED makers expanding to meet backlighting demand

LED-backlit TVs to reach 20% of 180m-unit LCD TV market in 2010

HB-LEDs to drive doubling of MOCVD sales to 415 systems in 2011

![]() Search: LCD TV backlighting LEDs MOCVD systems GaN

Search: LCD TV backlighting LEDs MOCVD systems GaN

Visit: www.researchinchina.com

![]() ©2010 Juno Publishing and Media Solutions Ltd. All rights reserved. Semiconductor Today and the editorial material contained within it and related media is the copyright of Juno Publishing and Media Solutions Ltd. Reproduction in whole or part without permission from Juno Publishing and Media Solutions Ltd is forbidden. In most cases, permission will be granted, if the author, magazine and publisher are acknowledged.

©2010 Juno Publishing and Media Solutions Ltd. All rights reserved. Semiconductor Today and the editorial material contained within it and related media is the copyright of Juno Publishing and Media Solutions Ltd. Reproduction in whole or part without permission from Juno Publishing and Media Solutions Ltd is forbidden. In most cases, permission will be granted, if the author, magazine and publisher are acknowledged.

Disclaimer: Material published within Semiconductor Today and related media does not necessarily reflect the views of the publisher or staff. Juno Publishing and Media Solutions Ltd and its staff accept no responsibility for opinions expressed, editorial errors and damage/injury to property or persons as a result of material published.

Semiconductor Today, Juno Publishing and Media Solutions Ltd, Suite no. 133, 20 Winchcombe Street, Cheltenham, GL52 2LY, UK

Web site by No Name No Slogan ![]()