- News

1 August 2018

Defense and 5G to propel RF GaN market past $1bn

© Semiconductor Today Magazine / Juno PublishiPicture: Disco’s DAL7440 KABRA laser saw.

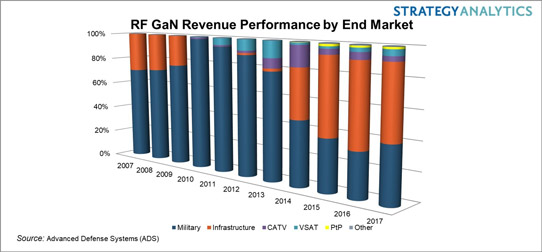

RF gallium nitride (GaN) market growth continued to accelerate in 2017 and, with revenues growing at over 38% year-on-year, will exceed $1bn by 2022 (with defense sector demand slightly greater than commercial revenue), forecasts the Strategy Analytics Strategic Component Applications (SCA) group report ‘RF GaN Market Update: 2017–2022’. GaN is seeing adoption across a range of RF applications. Growth is driven primarily by the rollout of commercial wireless infrastructure coupled with demand from military radar, electronic warfare (EW) and communications applications.

RF GaN demand from the military sector grew by 72% year-on-year in 2017, and the compound annual average growth rate (CAAGR) will be 22% through 2022. The military radar segment will remain the largest user of GaN devices in the defense sector. Substantial production activity in active electronically scanned array (AESA) radars for land-based and naval systems in particular is driving increasing demand for RF GaN, as many systems previously in development move to production.

“As well as demand from military radar, operational requirements to operate in contested and congested environments, as well as being able to counter modern agile radar and communications, will drive opportunities for RF GaN for the electronic warfare market,” notes Asif Anwar, director of the Advanced Defense Systems (ADS) service. “Communicating voice, data and video simultaneously and securely over wider and higher bandwidths in an increasingly complex spectrum environment will underpin trends for military communications system design,” he adds. “We expect the associated component demand will also be increasingly underpinned with RF GaN.”

Wireless base stations continue to be the single largest revenue segment for RF GaN, with increasing penetration translating to year-on-year growth of more than 20%. While the big boost from Chinese LTE deployments is over, the wireless industry has done a very good job of maintaining and, in some cases, compressing the 5G deployment schedule, says the report. The resulting 5G base-station deployment will become a primary commercial growth driver for RF GaN.

“GaN improves high frequency, instantaneous bandwidth, linearity and environmental performance capabilities and this allows equipment manufacturers to develop higher-capacity, higher-power and higher-performance radios,” notes Eric Higham, service director, Advanced Semiconductor Applications (ASA) service. “5G deployment will drive opportunities for GaN on multiple fronts, with demand coming from both fixed and mobile applications, operating below 6GHz, as well as in Ka-band and higher millimeter-wave frequency bands. Opportunities are also growing for RF GaN devices in wireless backhaul and VSAT, and we are seeing traction in the adjacent RF Energy market also.”

Qorvo saw good growth in its defense-related GaN revenue to maintain the market leader spot, widening the gap over rivals competing in the defense sector including captive suppliers such as Raytheon and Northrop Grumman. Sumitomo Electric Device Innovations (SEDI) continued to be the leading supplier to the overall RF GaN market in 2017, based largely on its dominant position in the base-station market, with Cree’s Wolfspeed maintaining second place.

The future continues to look promising for RF GaN adoption, even as growth drivers remain in flux, concludes Strategy Analytics.

www.strategyanalytics.com/access-services/components/