- News

21 June 2016

Finisar's growth in 100G datacom transceivers outweighs drop in legacy 10G telecom products

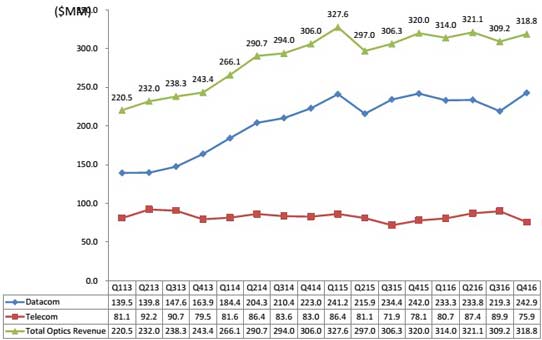

For fiscal fourth-quarter 2016 (ended 1 May), fiber-optic communications component and subsystem maker Finisar Corp of Sunnyvale, CA, USA has reported revenue of $318.8m, down slightly on $320m a year ago but up 3.1% on $309.2m last quarter.

Growth was driven mainly by demand for 40G and 100G transceivers (including CFP, CFP2, CFP4, QSFP and QSFP28 form factors). Datacom product sales were hence $242.9m, up 10.8% on $219.3m last quarter (and surpassing the previous record of $242m a year ago).

Telecom product sales were $75.9m, down 15.6% on $89.9m last quarter (and less than the $78.1m a year ago), primarily as a result of the full three months of the telecom price negotiations and an unexpected decline in demand for legacy products (including 10G fixed-wavelength and tunable transceivers and amplifiers). In addition, factors expected to partially offset the negative impacts on telecom revenue were weaker than expected due to delays in adding manufacturing capacity for wavelength-selective switches (WSS) and delays in the qualification of new reconfigurable optical add-drop multiplexer (ROADM) line-card designs.

Full-year revenue was $1263.2m, up 1% on $1250.9m in fiscal 2015, as a drop of $4.2m in datacom product sales fell by (due mainly to having only 52 weeks in the fiscal year compared to 53 weeks in fiscal 2015) was offset by a $16.4m rise in telecom product sales (driven mainly by growth in demand for wavelength-selective switches).

Graphic: Finisar's quarterly revenue trends.

On a non-GAAP basis, full-year gross margin was 30.3%, down from 30.9% in fiscal 2015 due to lower average selling prices. However, fiscal Q4 gross margin was 30.6%, up from 30.3% last quarter (and above the expected 30%), as favorable product mix offset the impact of the full three months of annual telecom price negotiations (which typically take effect on 1 January).

Operating expenses have been cut further, from $68.2m a year ago and $67.3m last quarter to $66.2m (better than the expected $67.5m), due mainly to lower general & administrative (G&A) costs (including lower legal expenses).

Full-year operating income has fallen from $116.1m (operating margin of 9.3% of revenue) in fiscal 2015 to $112.3m (8.9% of revenue) for fiscal 2016. However, quarterly operating income was $31.2m (operating margin of 9.8% of revenue, above the expected 8.2-9.2%), up from $26.3m (8.5% of revenue) last quarter.

Full-year net income $109.8m ($1.01 per fully diluted share), down from $110.4m ($1.04 per fully diluted share) in fiscal 2015. However, fiscal Q4 net income was $31.8m ($0.29 per diluted share), up from $26.6m ($0.25 per diluted share) last quarter.

"Better-than-expected gross margin, due to favorable product mix, and lower expenses resulted in earnings per fully diluted share exceeding the upper end of our prior guidance range [of $0.22-0.28]," notes executive chairman & CEO Jerry Rawls.

Capital expenditure (CapEx) has dropped further from an already lower-than-targeted $26.8m last quarter to $20m after delays in both some of the final CapEx associated with the fit out of the firm's second building in Wuxi, China as well as CapEx associated with expanding capacity for wavelength-selective switches.

Cash, cash equivalents and short-term investments has risen from $490.2m at the beginning of fiscal 2016 and $531.1m at the beginning of fiscal Q4/2016 to $562.5m at the end of fiscal Q4/2016.

For fiscal first-quarter 2017, Finisar expects revenue to rise to $323-343m (with both datacom and telecom revenue growing, although 40G will be relatively flat). The firm expects gross margin to grow to 31%.

Operating expenses should rise to $68.5m (due mostly to higher legal expenses from a patent trial where Finisar is the plaintiff). Finisar also expects an increase in payroll taxes from the annual vesting of employee RSU grants (which occurs every June). Despite this, operating margin should rise to 9.9-10.9%. Earnings per fully diluted share should be $0.27-0.33. Capital expenditure is expected to rise to about $30m.

"We continue to see strong demand from China due to the long-haul wireless build-outs at all of the major carriers," says Rawls. "North America demand remained strong due to the expansion of next-generation metro networks. Europe and Middle East demand is also strong," he adds.

Datacom revenue growth should be mainly from increased sales of 100 Gigabit Ethernet transceivers. Telecom revenue growth should be mainly from continued strong demand for wavelength-selective switches, 10G tunable transceivers and ROADM line-cards. In addition, revenue for 100G and 200G line-side product (such as CFP2-ACO) is expected to increase.

"We are experiencing such strong demand for our broad range of our product lines that we have many capacity constraints; we are actively adding capacity to try to meet our customer's demands," notes Rawls. "In our fiscal 2017, we expect to benefit from the ramp up of many new products," he adds. "Revenue growth will be driven by both data-center construction and upgrades as well as increased deployment of ROADMs and a 100G and 200G coherent transceivers in telecom networks."

Finisar's profits fall after higher-than-expected costs from new-product qualifications

Finisar's quarterly revenue grows despite annual telecom price reductions

Finisar opens production plant in Wuxi, China